Did you know that 94 percent of small businesses struggle with financial challenges, per the latest Main Street Metrics report? Yet, nearly half say they’re profitable. This is the impact of cash flow. Your business can be profitable and still feel daily strain when the money coming in doesn’t line up with the money going out. Thankfully, you can make educated predictions about the alignment of inflows and outflows and use the information to relieve the strain. In this guide, we’ll walk you through how to create these projections, plus share cash flow forecasting tips and some common mistakes to avoid.

Key Benefits of Cash Flow Forecasting

A cash flow forecast answers the question: “Will my business have enough cash to meet its obligations as they come due?” Knowing the answer translates into better business outcomes, which makes forecasting one of the best financial skills leaders can have.

A cash flow forecast answers the question: “Will my business have enough cash to meet its obligations as they come due?” Knowing the answer translates into better business outcomes, which makes forecasting one of the best financial skills leaders can have.

Forecasting Gives You Visibility into Your Cash Position

Even strong revenue can mask underlying cash constraints due to timing differences between receivables and payables.

- Early Identification of Cash Gaps: A forecast shows when outgoing payments are expected to exceed incoming cash so you can act before a shortfall hits.

- Proactive Financial Adjustments: You can adjust payment timing, accelerate collections, or secure funding in advance rather than reacting under pressure.

You Can Use the Data for More Informed Decision-Making

A structured forecast provides measurable insight and can improve the quality of your financial decisions.

- Data-Driven Growth Decisions: You can evaluate whether your cash position supports hiring, inventory purchases, or expansion.

- Clear Evaluation of Payment Terms: You can measure how extended payment terms or discounts affect liquidity.

A Realistic Cash Flow Forecast Gives You Stronger Financial Credibility

Consistent forecasting demonstrates financial discipline and improves how your business is perceived by external stakeholders.

- Improved Financing Position: Lenders and funding partners assess your ability to manage cash flow when evaluating risk. Your forecast backs you up and can help you maximize funding.

- Greater Negotiation Leverage: When funding is part of a clear plan, you’re better positioned to secure favorable terms.

You Can Use Your Projections to Create Alignment Between Cash Flow and Business Growth

Because growth often widens the gap between inflows and outflows, an operating cash flow forecast helps ensure expansion remains sustainable.

- Planned Scaling: You can map how increased revenue impacts payroll, supplier payments, and operating costs.

- Defined Working Capital Strategy: You can identify when to introduce tools such as invoice factoring to maintain consistent liquidity.

How Forecasts Are Used in Small Business Cash Flow Management

As one of the most essential types of financial forecasting, cash flow projections function as an ongoing cash flow management tool that supports both day-to-day operations and long-term planning.

Manage Day-to-Day Cash Flow

At the operational level, your forecast helps ensure that core obligations are consistently met.

- Short-Term Cash Planning: You track expected inflows and outflows to confirm that payroll, vendor payments, and recurring expenses are covered.

- Payment Timing Control: You can sequence outgoing payments in a way that aligns with expected incoming cash.

Plan for Different Scenarios

Forecasting allows you to evaluate how changes in your business environment affect your cash position, such as by performing a cash flow stress test.

- Scenario Analysis: You can model outcomes such as delayed customer payments or increased expenses and assess their impact on liquidity.

- Risk Mitigation Planning: You can prepare responses in advance, such as adjusting expenses or arranging access to funding.

Guide Strategic Decisions

A forecast provides the financial clarity needed to time major business decisions effectively.

- Timing of Investments: You can plan capital expenditures, marketing initiatives, or expansion based on projected cash availability.

- Evaluation of Funding Needs: You can determine when to use financing tools, including lines of credit or factoring, to support operations.

Improve Budgeting and Cash Flow Planning

Forecasting also serves as a feedback mechanism that allows you to strengthen financial management over time.

- Forecast Versus Actual Analysis: You compare projected cash flow to actual results to identify patterns such as slow-paying customers or rising costs.

- Continuous Refinement: Each forecasting cycle improves accuracy, leading to more reliable planning and stronger decision-making.

Direct vs. Indirect Cash Flow Forecasting

There are two main types of cash flow forecasting: direct and indirect. It’s helpful to know the difference and when each works best.

Direct Cash Flow Forecasting

Sometimes referred to as a “bottom-up” approach, direct cash flow forecasting involves listing expected cash inflows and outflows by category, such as customers, payroll, and vendor payments.

This allows for a high degree of accuracy and granular visibility into cash timing, so you can ensure you have sufficient funds to meet immediate obligations. However, it is labor-intensive plus requires detailed data from your bank accounts, accounts receivable, and accounts payable. For this reason, it’s typically only used for short-term forecasting, such as weekly or monthly projections.

Indirect Cash Flow Forecasting

Referred to as the “top-down” approach, indirect cash flow forecasting starts with projected net income and then adjusts for non-cash transactions and working capital changes.

This method only requires data from your existing financial statements, so it’s easier to produce. However, it doesn’t provide the same level of granularity and accuracy as the direct method, so it’s not ideal for short-term or day-to-day cash management. It’s typically used for long-term strategic forecasting and budgeting, such as monthly, quarterly, or yearly projections.

How to Forecast Cash Flow for a Small Business

While there are many approaches, and your decision to use the direct vs. indirect method will impact complexity, creating a small business cash flow forecast is easier than most expect.

Step 1: Define Your Forecast Period

Start by choosing the time horizon and level of detail for your forecast. As touched on earlier, this determines how actionable it will be.

- Select a Time Frame: Most small businesses use a 13-week rolling forecast for short-term planning. For strategic decisions, a six or 12-month forecast may be more ideal.

- Match Detail to Your Needs: Weekly forecasting works well for businesses with tight cash cycles, such as those in trucking, staffing, manufacturing, oil and gas services, and professional services. Meanwhile, monthly forecasting may be sufficient for operations with more stable cash flow.

Step 2: Estimate Cash Inflows

Cash inflows represent the money you expect to receive, based on actual payment behavior.

- Base Projections on Payment Timing: Use historical data to estimate when customers actually pay. For example, if your terms are net 30 but customers pay in 45 days on average, your forecast should reflect 45 days.

- Include All Cash Sources: Account for customer payments, recurring revenue, financing proceeds, and any one-time inflows such as asset sales or tax refunds.

Step 3: Estimate Cash Outflows

Outflows include all expenses and obligations that require cash payments.

- List Fixed and Variable Expenses: Fixed costs include rent, payroll, and insurance. Variable costs include materials, shipping, and commissions that fluctuate with revenue.

- Capture Timing of Payments: Record when payments are due, not when expenses are incurred.

Step 4: Calculate Net Cash Flow

Once you forecast cash inflows and outflows, you can calculate the net change in cash for each period.

- Measure Period Cash Movement: Subtract total outflows from total inflows for each week or month to determine whether cash is increasing or decreasing.

- Track Cumulative Cash Position: Add each period’s net cash flow to your starting balance to see how your total cash position evolves over time.

Step 5: Identify Gaps and Pressure Points

Next, check your numbers for any signs of trouble.

- Pinpoint Timing Gaps: Look for periods where cash balances drop below your comfort level or approach zero.

- Assess Operational Risk: Identify whether shortfalls are driven by slow receivables, high expenses, or rapid growth.

Step 6: Build Scenarios

Knowing what you expect to happen is a good start, but forecasts can also be used to explore what-ifs and plan for those, too.

- Model Different Outcomes: In addition to your expected forecast, create forecasts that represent different situations, such as what might happen if you have slower collections or higher expenses.

- Quantify Impact on Cash: Evaluate how each scenario affects your ability to cover obligations and maintain operations.

Step 7: Update and Refine Regularly

Strengthen your financial habits. Keep using and refining your forecast to improve accuracy over time.

- Compare Forecast to Actual Results: Review differences between projected and actual cash flow to identify patterns, such as consistently late payments.

- Adjust Assumptions Over Time: Update your inputs based on real performance so your forecast becomes more accurate with each cycle.

Simple Cash Flow Forecast Example

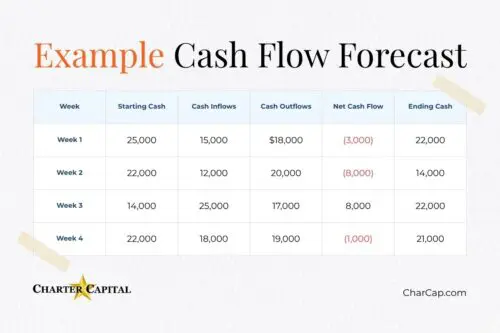

Next, let’s take a look at an example that uses the direct cash flow forecasting method.

As you can see in this cash flow forecast example, it’s easy to identify:

- Short-Term Cash Pressure: Week two shows a significant drop in ending cash due to lower inflows and higher outflows.

- Recovery Periods: Week three reflects a large inflow that restores the cash position.

- Ongoing Variability: Cash balances fluctuate week to week in this example. This is quite common for small businesses, with half saying uneven cash flow is one of their key financial challenges, per the latest Small Business Credit Survey. This also highlights why cash flow forecasting, particularly using shorter intervals, is crucial for financial health.

10 Essential Cash Flow Forecasting Tips and Strategies for Improving Cash Flow Projections

Once you have the basics down, you can begin applying tips to improve accuracy and make your forecast more actionable.

1. Equip Yourself with the Right Cash Flow Tools for Small Businesses

If you’re just getting started, you can create a forecast with nothing more than a spreadsheet and your data. However, you’ll get faster, more accurate results if you’re leveraging accounting software that provides reporting tools. Some also have add-ons that will perform projections for you, such as Xero with the Xero Analytics Plus upgrade. Or, you can purchase specialized software that integrates with your current payment and accounting technology, such as Cash Flow Frog, Fathom, or Float.

2. Use Actual Timing

Make sure your projections reflect the reality of your business. Your cash flow projections should always use the actual dates money arrives and the dates payables are due, regardless of when invoicing occurs or the balance is generated.

3. Keep the Forecast Rolling

Maintain a rolling forecast and update it regularly so you always have a current view of your cash position. For instance, if you operate a small business and cash flow is tight, you may want to create a new 13-week cash flow forecast every week.

4. Separate Fixed and Variable Costs

Your variable costs change with the normal ebb and flow of business, while your fixed costs hold steady. Splitting them makes it easier to perform a break-even analysis, assess scalability, spot opportunities for improvement, and more.

5. Forecast Inflows Conservatively

Apply slightly cautious assumptions to incoming cash to reduce the risk of overestimating available funds.

6. Review Forecast Versus Actuals

Compare projected cash flow to actual results each cycle to identify patterns and refine your assumptions over time.

7. Incorporate Seasonality

Account for predictable shifts in revenue or expenses throughout the year so your forecast reflects how your business actually operates.

8. Include One-Time Events

Add known large inflows or outflows, such as equipment purchases or tax payments, so they do not distort your cash position unexpectedly.

9. Build a Minimum Cash Threshold

Define a baseline cash level your business should maintain, and use your forecast to monitor when balances approach that threshold. Determine in advance what you’ll do when that threshold is met, so you can respond quickly and confidently if it happens.

10. Align Forecast with Decision-Making

Use your forecast to guide timing for hiring, inventory purchases, investments, and other large expenses to ensure they don’t create unnecessary strain.

Common Mistakes to Avoid in Cash Flow Forecasting

Next, let’s take a look at some of the most common mistakes business owners make when creating a cash flow forecast, so you can avoid them and improve the accuracy and usefulness of your projections.

Confusing Sales with Cash Received

Always base your forecast on expected payment dates. A sale does not improve cash flow until the money is collected.

Using Payment Terms Instead of Payment History

If your invoices are due in 30 days but customers usually pay in 45 days, your forecast should reflect 45 days to ensure accuracy.

Leaving Out Irregular Expenses

Annual insurance premiums, tax payments, equipment repairs, and software renewals can create unexpected pressure if they are missing from the forecast. Include known one-time and seasonal costs.

Overestimating Incoming Cash

It’s safer to forecast customer payments conservatively, especially when payment timing is uncertain.

Underestimating Growth Costs

Growth often requires cash before revenue is collected. Payroll, materials, inventory, and vendor payments may rise before customer payments arrive.

Ignoring Seasonality

Many businesses experience predictable shifts in sales, expenses, or customer payment behavior throughout the year. A flat forecast can miss those patterns.

Having a Set-it-and-Forget-it Mentality

Review your forecast regularly against actual results and adjust assumptions as conditions change. Remember to use it when you’re making decisions about spending, collections, hiring, inventory, and funding.

Forgetting to Build in a Cash Cushion

Operating too close to zero leaves little room for delayed payments or unexpected expenses. Establish a minimum cash threshold and monitor when the forecast approaches it.

Failing to Establish Backup Funding Based on Your Cash Flow Forecast

Even if you avoid cash flow mistakes, rapid growth, slow customer payments, and emergencies can change your cash position overnight. It’s essential to know what your threshold for action is in advance and have a backup form of funding ready to go when you reach it.

For businesses that invoice other businesses (B2B) after goods or services are delivered, invoice factoring may be the ideal solution. You can become established with a factoring company in advance and not use their services until you project a shortfall. When you predict a cash flow gap, you can then submit your unpaid invoices to the factoring company to receive immediate payment for most of the invoice’s value. They’ll even take care of collecting for you.

With small business factoring, no debt is added to your balance sheet, and no interest is accrued, as you’re simply accelerating your cash inflows by eliminating the wait for customer payment.

Strengthen Your Cash Flow with Charter Capital

Whether you need to accelerate inflows on an ongoing basis or simply want to ensure you’re set up for success should your projections predict a cash flow gap in the future, we can help. As a leading invoice factoring company for more than 25 years, Charter Capital makes factoring simple with a fast and easy approval process, same-day funding, and competitive rates. To explore the fit more or get started, request a no-obligation rate quote.

FAQs About Cash Flow Forecasting for Small Businesses

How often should a small business update its cash flow forecast?

Most small businesses benefit from updating their cash flow forecast on a weekly basis, particularly when cash cycles are tight or payment timing is unpredictable. A rolling 13-week forecast, refreshed each week, gives you a consistent view of your short-term cash position. Businesses with more stable cash flow may find monthly updates sufficient, but weekly reviews improve accuracy and allow faster responses to emerging gaps.

What data sources should a small business use to build a cash flow forecast?

The most reliable data sources for a cash flow forecast are your accounts receivable aging report, accounts payable schedule, bank statements, and payroll records. These reflect actual payment timing rather than invoice dates or contract terms. For businesses that have operated for at least one full year, historical payment data by customer is especially useful for estimating realistic inflow timing.

What is the difference between short-term and long-term cash flow forecasting?

Short-term cash flow forecasting typically covers a period of 13 weeks or less and uses the direct method, tracking expected inflows and outflows at a transaction level. Long-term forecasting covers six to twelve months and generally uses the indirect method, starting from projected net income and adjusting for working capital changes. Short-term forecasts support daily operations; long-term forecasts support budgeting and strategic planning.

How do timing gaps between invoices and customer payments affect forecast accuracy?

Timing gaps are one of the most common sources of forecast inaccuracy. When a business uses invoice due dates rather than actual customer payment history, the forecast overstates available cash. For example, if your terms are net 30 but customers consistently pay in 45 days, building your forecast on 30-day timing creates a 15-day gap that can trigger shortfalls. Accurate forecasting requires using real payment behavior, not contractual terms.

How do you determine the right minimum cash threshold for a small business?

A minimum cash threshold should cover your highest-cost week of fixed obligations, including payroll, rent, and any recurring vendor payments, with a buffer for delayed customer payments. Many small businesses set their threshold at two to four weeks of core fixed expenses. The key is to define the threshold in advance and establish a plan for how you will respond when your forecast shows the balance approaching it.