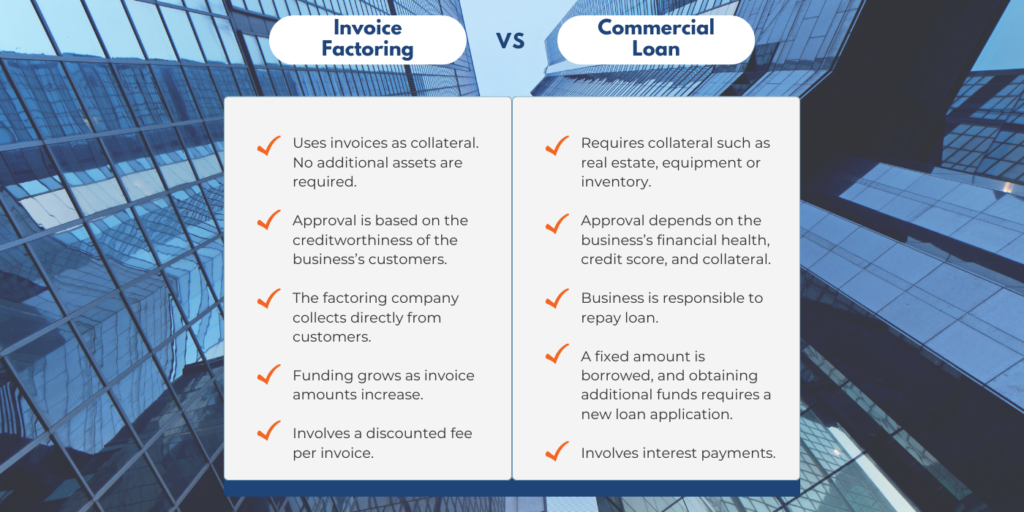

Companies comparing a commercial loan vs. invoice factoring will typically find that factoring is more accessible, flexible, and faster. Unlike commercial loans and alternative financing options, invoice factoring is not a loan, creates no debt, and is repaid when the customer pays the invoice, which makes it ideal for businesses that want to preserve their credit and stabilize cash flow. Plus, when working with a factoring company like Charter Capital, you’ll receive free collections services, competitive rates, and other benefits that make it easier to grow and thrive.

Commercial Loan vs. Invoice Factoring: Comparison at a Glance

Factoring can help you raise immediate cash for any purpose your business may have, from operations to payroll. The effectiveness, speed, and flexibility of factoring have made the process a preferred non-loan alternative to commercial loans.

Quick Comparison: Invoice Factoring vs. Business Loan

| Invoice Factoring | Commercial Loan | |

|---|---|---|

| How it Works | Selling unpaid B2B invoices to a factoring company for immediate payment | Receiving a lump sum of cash upfront that requires repayment |

| Repayment | Balance is cleared when your customer pays their invoice | Typically made in monthly installments regardless of your cash flow |

| Primary Approval Criteria | Creditworthiness of your customers | Your creditworthiness |

| Debt Impact | None | Adds debt and interest to balance sheet |

| Speed | Same-day funding available | Usually takes weeks or months |

| Contract Flexibility | No long-term contract required | Contracts typically last years |

| Additional Perks | Collections services and business funding or growth resources | None |

How Commercial Loan and Factoring Services Differ

While both factoring and commercial loans can provide businesses with working capital to support operations, they work in different ways.

Commercial Invoice Factoring Lets You Access Money You’ve Earned Faster

Sometimes referred to as accounts receivable factoring or AR factoring, invoice factoring is a service that’s typically provided through invoice factoring companies, also known as factors. It’s typically used as a cash flow management tool, though it can also serve as an alternative to traditional loans.

With factoring, you submit your unpaid business-to-business (B2B) invoices to the factor and receive most of the invoice’s value right away. At Charter Capital, that’s up to 100 percent of the value of your invoice, minus the factoring fee, in your bank account as quickly as the day you submit your invoice. We collect the balance from your customer for you, then send you the residual after your customer pays. There’s no debt created and no interest to pay back.

Because there’s no interest, the cost of factoring is mostly determined by your factoring rate, which is calculated as a percentage of the invoice’s value. This is usually between one and five percent of an invoice’s value, depending on the factor, though at Charter Capital, most of our clients sit around three percent.

Invoice Factoring vs. Invoice Financing

It’s worth noting that invoice factoring should not be confused with invoice financing. While both are invoice funding solutions that provide working capital based on the value of your receivables, factoring doesn’t create debt because you’re selling the invoice to the factor. Invoice financing is a loan that uses receivables as collateral, which you pay back with interest.

Invoice Factoring vs. Line of Credit

Invoice factoring shares several traits with business lines of credit. For instance, both allow you to tap into funding as needed, your limit can scale, and, depending on the nature of your agreement, you may not pay anything to have the funds available; fees often only accrue when you leverage the funding tool.

However, a line of credit still creates debt that your business must pay back with interest, and approval is largely contingent on your creditworthiness. Factoring doesn’t have the same rigid approval requirements, doesn’t create debt, and actually relieves you of back-office burden by taking care of collections for you.

Invoice Factoring vs. Cash Flow Loans for Businesses

Invoice factoring and cash flow loans both provide funding for your working capital needs, but they do it in different ways. Cash flow loans work like most business loans; you receive a lump sum that you have to pay back with interest. Factoring doesn’t create debt and there’s nothing to pay back because the balance is cleared when your customer pays their invoice.

Commercial Loans Provide a Lump Sum You Pay Back with Interest

Commercial loans, also called business loans, are a type of traditional financing. They’re typically offered through banks, credit unions, and online lenders.

With commercial loans, you receive a lump sum, then pay it back in installments with interest. Interest rates on business loans typically sit between six and 11 percent when you work with a bank or have a Small Business Administration (SBA) loan, though online lenders tend to charge more.

Key Benefits of Commercial Factoring vs. Commercial Business Loans

Because factoring works differently from commercial loans, it stands out in a number of ways.

Easier Approval Than Working Capital Loans for Businesses

Most businesses that apply for commercial loans are not fully approved. There’s lots of red tape, ranging from minimum credit scores to revenue requirements and time in business. Meanwhile, approval for factoring is largely based on the creditworthiness of your customers, as they’re the ones responsible for paying the invoices. You can qualify if your business is young. In fact, Charter Capital even works with startups, provided you’re actively invoicing B2B clients.

Approval Process of Invoice Factoring vs. Business Loan

| Invoice Factoring | Commercial Loan | |

|---|---|---|

| Financial Statements Needed | No | Yes |

| Dependent on Personal Credit | No | Yes |

| Must Provide 3 Years of Tax Records | No | Yes |

| Lengthy Approval Process | No | Yes |

| Denied for IRS Problems – Tax Liens | No | Yes |

Faster Funding for All Your Short-Term Business Financing Needs

Those seeking fast business loan approval are often left disenchanted by traditional lenders because approval can take weeks or months, which significantly delays the payment timeline. Conversely, factoring can come through in days. At Charter Capital, you can receive your factoring quote and terms on the day you apply. We offer same-day funding, too.

More Flexibility Than Typical Business Loans for Growing Companies

It’s easier to tailor your agreement to how you operate with factoring. The cash available also increases as your invoice volume grows, unlike loans. Plus, at Charter Capital, you can factor as much as you like, whether you want to factor only occasionally or all your invoices, and you aren’t tied into a long-term contract.

Greater Accessibility Than Common Financing Options for Established Businesses

Factoring tends to suit businesses with strong commercial customers but limited credit history or collateral.

Types of Businesses Funded by Commercial Loan vs. Invoice Factoring

| Invoice Factoring | Commercial Loan | |

|---|---|---|

| Fast Growth | Yes | No |

| Startups | Yes | No |

| Profitable with No Capital | Yes | No |

| Financial Losses | Yes | No |

| Seasonal | Yes | No |

Your Non-Bank Business Financing Comes with Additional Support

Collections are taken care of for you when you factor. There’s no additional fee for this for Charter Capital clients, and everything is managed in an easy-to-use digital portal.

We also tailor our small business factoring services to support the needs of specific industries, such as trucking and freight services, staffing, security, professional services, manufacturing, and oil and gas services. For instance, our trucking clients can receive a fuel card that makes managing top-offs easier (product not available in California).

Program Features of Commercial Factoring vs. Business Loans

| Invoice Factoring | Commercial Loan | |

|---|---|---|

| Unlimited A/R Funding | Yes | No |

| No Financial Covenants | Yes | No |

| Advances Up to 98% | Yes | No |

| Free Credit Checks | Yes | No |

| A/R Management | Yes | No |

Get Business Funding without a Bank Loan with Charter Capital

If commercial loans are out of reach, you don’t want to take on debt, or you require cash quicker than a commercial loan can provide, factoring may be the solution you’re looking for. Charter Capital has been making factoring simple for small and mid-sized businesses for decades, and we welcome the opportunity to help your company level up, too. To learn more or get started, request a no-obligation rate quote.

FAQs on Invoice Factoring vs. Business Loan

Is invoice factoring better than a business loan?

Invoice factoring is not necessarily better than a business loan, but it may be a better fit depending on your business’s needs. Business loans provide a lump sum that must be repaid over time, while factoring converts unpaid invoices into immediate working capital.

Factoring can be advantageous for businesses with strong receivables, rapid growth, or cash flow gaps caused by long customer payment terms. Loans may be more appropriate for major purchases, long-term investments, or businesses without a steady stream of invoices.

The best option depends on your cash flow needs, credit profile, and funding goals. Many businesses choose factoring because it provides access to capital without adding traditional debt to the balance sheet.

Is invoice factoring a type of commercial loan?

Absolutely not. Even though the process of accounts receivable factoring is sometimes referred to as “factoring loans,” it is not a loan, but is a financial transaction between the business seeking funds and factoring companies. There is no bank involved. Accounts receivable factoring (invoice factoring) is when a company, like Charter Capital, purchases your accounts receivable invoices at a discount rate and provides you with immediate cash.

Factoring can be a great alternative to traditional loans. It gives your business access to quick cash flow and is a funding solution that is instant and unlimited. The use of accounts receivable factoring means that your open customer invoices (accounts due) are “cash in the bank.”

How is invoice factoring different from a commercial loan?

When comparing a commercial loan vs. invoice factoring, businesses often find that invoice factoring offers faster approval, more flexible terms, and no debt on the balance sheet. Unlike commercial loans that require extensive financial statements, three years of tax records, and strong personal credit, Charter Capital provides same-day funding based on your customers’ creditworthiness, with advances up to 98 percent of invoice value. Our invoice factoring solutions serve fast-growing businesses, startups, seasonal companies, and those facing financial challenges that would be denied traditional bank financing.

Are accounts receivable factoring companies an alternative to a commercial loan for business funding?

As an alternative source of business financing, invoice factoring eliminates many of the difficult-to-meet criteria that companies must face in order to get a commercial loan. If you can get a loan or line of credit in today’s tight banking market, what’s going to happen after you’ve depleted those funds? You will still have to wait for the outstanding invoices to be paid. The biggest problem with a traditional bank loan is that there is a maximum credit limit.

In comparison, Charter Capital provides no-loan cash based on the quality and liquidity of your assets (your accounts receivable). Because each account is evaluated individually, Charter Capital has much more flexibility than a Bank regarding keeping up with an increase in sales. This means that businesses can access a larger amount of working capital than traditional loans to support growth. Charter Capital also offers a much faster approval process and offers same-day funding.

Is it easier to qualify for factoring or a commercial loan?

Less than 40 percent of businesses that apply for business loans are fully approved, per the Federal Reserve Banks. This is because banks have rigid criteria. For instance, those applying for U.S. Small Business Administration (SBA) and bank loans must have a credit score of at least 680, the Office for Financial Regulation reports. Factoring doesn’t have this requirement, so it’s easier to get approved.

How are commercial finance and factoring different?

Commercial finance is a broad category of business funding solutions that help companies manage cash flow, purchase equipment, finance growth, or support operations. It includes products such as business loans, lines of credit, asset-based lending, equipment financing, and invoice factoring.

Factoring is one type of commercial finance. Instead of borrowing money, a business sells its unpaid invoices to a factoring company in exchange for an immediate cash advance. The factor then collects payment from the customer when the invoice comes due.

In short, commercial finance refers to a wide range of funding options, while factoring is a specific solution that turns outstanding invoices into working capital.

What are the alternatives to traditional invoice factoring?

Several factoring alternatives can help businesses improve cash flow, including business lines of credit, term loans, merchant cash advances, equipment financing, and asset-based lending. Each option has different qualification requirements, costs, and repayment structures.

When evaluating a specific invoice factoring alternative, it’s important to consider how quickly funds are available and whether the solution adds debt to your balance sheet. Unlike many financing products, invoice factoring provides immediate access to working capital by leveraging outstanding invoices rather than requiring businesses to take on additional debt.

The right choice depends on your cash flow needs, credit profile, and growth plans. For companies with strong receivables and long customer payment terms, factoring often remains one of the most flexible funding solutions available.

How can I avoid a CI for a loan?

Avoiding a credit inquiry can be challenging because most lenders review your credit history as part of the loan approval process. While some lenders offer prequalification with a soft credit check, a hard inquiry is typically required before funding.

If avoiding a credit inquiry is a priority, you may want to consider alternatives to traditional loans. Invoice factoring, for example, is based primarily on the value of your outstanding invoices and the creditworthiness of your customers rather than your personal credit profile. As a result, many businesses use factoring to access working capital without going through the same underwriting process required for conventional financing.

How is a loan invoice used?

A loan invoice is a document that outlines the amount borrowed, repayment terms, interest charges, and payment schedule associated with a loan. Lenders use it to record the details of the financing arrangement and track payments over time.

Businesses may receive loan invoices for equipment financing, commercial loans, or other forms of business funding. The invoice serves as a billing statement, showing what is owed and when payments are due.

Unlike a loan invoice, a standard customer invoice represents money owed to your business for products or services provided. These unpaid customer invoices can often be used to secure working capital through invoice factoring.

What makes factoring different than other alternative business lending solutions?

Factoring differs from many alternative business lending solutions because it is not a loan. Instead of borrowing money and repaying it with interest, businesses sell their unpaid invoices to a factoring company in exchange for an immediate cash advance.

Many financing options require fixed repayments and add debt to the balance sheet. Factoring converts existing accounts receivable into working capital, helping businesses improve cash flow without taking on additional debt. Approval is also often based more on the creditworthiness of your customers than your business’s credit history.

For companies that regularly issue invoices with extended payment terms, factoring can provide a flexible source of funding that grows alongside sales.