Accounts receivable factoring is an alternative funding solution that converts outstanding business-to-business (B2B) invoices into immediate working capital by selling them to a factoring company at a discount. By closing the gap between delivering goods or services and getting paid, AR factoring aligns inflows and outflows and stabilizes cash flow, providing growing businesses with the working capital they need to thrive. As a leading provider of accounts receivable factoring services for more than 25 years, Charter Capital offers businesses across the United States same-day payments, rates as low as one percent, and advances of up to 98 percent. We also provide tailored services for industries such as trucking and freight, temporary staffing, manufacturing, oil and gas services, security firms, and professional services, to help ensure your funding is just the right fit.

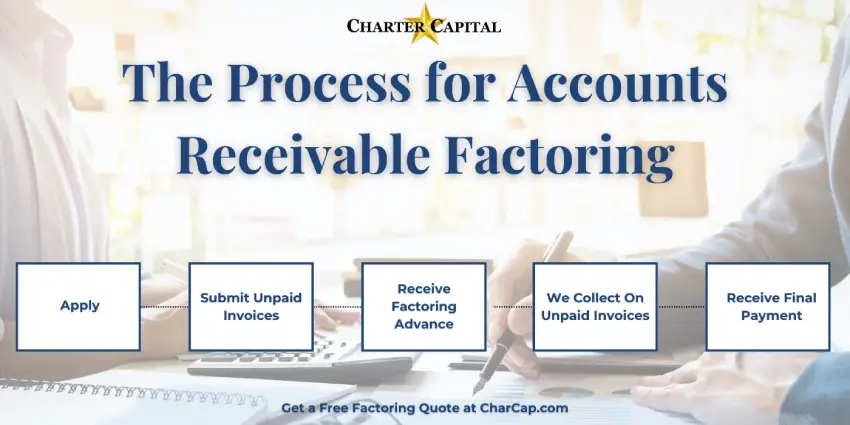

Factoring Receivables is a Simple Process

Although each provider may have slight variations, most accounts receivable factoring companies follow a process like the one outlined below. This is also what you can expect when you’re factoring accounts receivable with Charter Capital.

- Apply: To start, you’ll apply for an AR factoring account. Most B2B businesses can qualify, provided they have creditworthy customers and sufficient invoice volume.

- Begin Factoring Receivables: Once approved, you can begin submitting invoices to your AR factoring company.

- Receive Factoring Advance: You receive most of the invoice’s value right away. This is typically deposited directly into your bank account and typically arrives within 48 hours, though some factors, like Charter Capital, offer same-day payments.

- Focus on Your Core Operations: The collections process is taken care of for you, so you can focus on your business. Customers keep the payment terms you’ve set with them, though they remit payment to the account receivable factor instead.

- Receive Final Payment: Once the factor receives payment from your customer, the residual is sent to you, minus a small fee for the factoring service.

- Repeat as Needed: When you partner with an AR funding company like Charter Capital, there are no long-term contracts. You can factor as little or as often as you like.

Recourse vs. Non-Recourse Factoring of Accounts Receivable

There’s always some risk that factoring debtors, your customers, won’t pay an invoice. In a traditional factoring agreement, you factor your accounts receivable with recourse, which means the risk stays with your business with you. As an alternative to factoring receivables with recourse, you can opt for non-recourse factoring, which transfers risk to your factor.

Factoring Accounts Receivable with Recourse

When you factor receivables with recourse, and your customer doesn’t pay an invoice, you’ll be responsible for ensuring the factoring company doesn’t take a loss. This usually means you’ll submit a new invoice of equal or greater value in its place, although some factors will also leverage your reserve account or accept repayment instead.

Factoring Accounts Receivable without Recourse

In certain industries, receivables factoring with recourse leaves the business with too much risk. Non-recourse factoring eliminates the risk when a customer becomes insolvent, although the rates are typically higher to reflect the additional risk the factoring company is accepting.

Factoring Accounts Receivable Example

When you’re factoring account receivables, your customer pays on their usual terms, such as net 30 or net 60. Your account receivables factoring fee can land anywhere between one and five percent, though, at Charter Capital, it’s usually between one and three percent. Using these as inputs, a sample account receivable funding process, complete with advance rates and fees, is outlined below.

| Step | What Happens | Calculation | Amount |

|---|---|---|---|

| 1 | You submit a $30,000 invoice to Charter Capital | Invoice value | $20,000 |

| 2 | Charter Capital advances 95% to your bank account | $30,000 x 95% | $28,500 sent to you |

| 3 | A 2% factoring fee is calculated from the final invoice | $30,000 x 2% | $600 fee |

| 4 | Your customer pays in full | Full invoice paid in 30 days | $30,000 paid to Charter Capital by your Customer |

| 5 | Charter Capital releases the residual minus the fee | $30,000 – $28,500 – $600 | $900 sent to you |

| Total | $28,500 upfront + $900 on settlement = $29,400 total received | Total factoring cost | $600 (2% of $30,000) |

Getting Approved for Accounts Receivable Factoring is Easy

The requirements for factoring receivables are much different from getting approved for a bank loan. Instead of scrutinizing your business, years in operation, credit score, and other details that often result in loan denials, accounts receivable factoring companies focus more on the creditworthiness and payment histories of your customers.

If your business is actively generating invoices and your customers are overall strong payers, you’re likely to get approved for AR factoring.

Ensure Your Invoices Are Eligible for Factoring

While most businesses can qualify for receivable factoring, each invoice is assessed on its own merit. Account receivables factoring services are a better fit for businesses with invoices that meet the criteria below.

- Completed Work or Delivered Goods: You can only factor invoices for services you finished or products you’ve shipped. The service must also be fully accepted by the client.

- B2B or B2G Clients: Invoices must be billed to other businesses or government entities. Business-to-consumer (B2C) invoices won’t qualify.

- Creditworthy Customers: Your accounts receivable funding company will look at your customers’ credit. If your client has a strong track record of paying on time, the invoice is likely eligible.

- Short Payment Terms: Invoices with payment terms longer than 90 days typically don’t qualify for factoring. Most AR factors prefer standard 30-, 60-, or 90-day terms.

- Unencumbered Accounts Receivable: The invoice must be free of any liens. If another lender, like a bank or the IRS, has claimed your accounts receivable as collateral, the factor will need to obtain a subordination agreement before they can fund the invoice.

- No Disputes or Backlogs: Invoices must be clearly documented, accurate, and free of disputes. Past-due invoices or those older than 90 days generally don’t qualify.

There Are Many Benefits of Using Accounts Receivable Factoring Services

Business receivable factoring works differently from other funding solutions, so it’s more versatile and comes with unique benefits.

- Immediate Increase in Working Capital from Receivables: Factoring unlocks cash that’s trapped in your accounts receivable. This cash can be used for expenses like payroll and other business growth needs.

- No New Debt: Any balance is cleared when your customer pays their invoice, so no debt is added to your balance sheet.

- Predictable Cash Flow: By factoring accounts receivable, your inflows align more closely with delivering services or goods. You know exactly when you’ll get paid. Moreover, because there’s no debt to pay back when you factor receivables, finances often become more stable and easier to manage.

- Offer Better Credit Terms: You get paid right away, regardless of whether you’re offering your clients net-30 or net-90 payment terms. Many businesses offer their clients better terms to lock in more work or win bids.

- Go After Big Accounts: Many large corporations push vendors and subcontractors onto 90-day payment terms that can deplete cash and make it impossible to stay afloat. With accounts receivable factoring, you can bid on and accept these contracts with confidence.

- Take Advantage of Supplier Early-Pay Discounts: With the predictable cash flow provided by receivables factoring, you can take advantage of early-pay discounts, improve your credit rating, and offset the cost of factoring, all at the same time.

- Spend Less Time Managing Your Receivables: As experts in accounts receivable management, Charter Capital allows you to spend less time managing your receivables and more time managing your business.

- Receive Complementary Back-Office Support: As a business owner, you are continuously looking for ways to save costs. Reduce your overhead costs associated with managing your accounts receivable and processing payments. We will handle that for you.

Know Your Accounts Receivable Funding Tool: Accounts Receivable Financing vs. Accounts Receivable Factoring

Accounts receivable financing, sometimes called invoice financing or invoice discounting, is often confused with accounts receivable factoring, sometimes called invoice factoring. While both provide working capital based on the value of your invoices and are more accessible than traditional bank loans, AR financing is a form of asset-based lending. You’re taking out a loan that uses your invoices as collateral. You pay the balance back with interest and fees. Conversely, factoring is not a loan. There’s no debt or interest to pay back.

Receivables Financing vs. Factoring at a Glance

| AR Factoring | AR Financing | |

|---|---|---|

| How it Works | Selling unpaid B2B invoices to an account receivable factoring company for immediate payment | Your invoices serve as collateral on a loan that pays out as a lump sum or line of credit |

| Repayment | None; the balance is cleared when your customer pays their invoice | Typically made in monthly installments with full repayment often expected in 30 to 90 days |

| Primary Approval Criteria | Creditworthiness of your customers | Your creditworthiness and the quality of your invoices |

| Debt Impact | None | Adds debt and interest to your balance sheet |

| Speed | Same-day approval and same-day funding available | Setup takes a few days; payout typically occurs 24-48 hours later |

| Contract Flexibility | No long-term contract required | Contracts usually last between 1 and 3 years |

| Additional Perks | Receivables collection services and business funding or growth resources | None |

Charter Capital is a Leader in Accounts Receivable Factoring Companies

At Charter Capital, we set ourselves apart from other account receivable factoring companies in many ways, but ultimately, they all tie back to better service for our clients.

Why Factor Accounts Receivable with Charter Capital

- Transparency: We’re happy to walk you through the options before you apply. We also disclose all fees clearly up front, so you can make informed decisions about your business.

- Approval Speed: You can be approved for accounts receivable factoring on the day you apply.

- Same-Day Receivables Funding: Once you’re active, you can receive same-day payments.

- Competitive Terms: Our factoring rates start as low as one percent, and advances are as high as 98 percent.

- Flexibility: Unlike other AR factoring companies, Charter Capital requires no long-term contracts. You can also factor as much or as little as you need.

- Service: You’ll have a dedicated account manager available to support you as needed.

- Savings: In addition to our low factoring rates, you’ll benefit from no sign-up fees, free collections services, and free customer credit checks.

Hear Why People Think Charter Capital is the Best Accounts Receivable Factoring Company

Get Started with Fast Accounts Receivable Funding

If you’d like to explore how accounts receivable factoring services can streamline your cash flow and give your business the edge it needs to grow, connect with us for a no-obligation rate quote.

FAQs on Accounts Receivable Funding Solutions and Accounts Receivable Factoring Companies

How long does it take to get an accounts receivable cash advance?

The timeline for receiving an accounts receivable cash advance varies by provider, but many businesses can access funds within one to three business days after approval. Existing clients often receive advances even faster once their accounts are established.

Funding speed depends on factors such as the completeness of your documentation, invoice verification requirements, and the creditworthiness of your customers. In some cases, same-day funding may be available.

Compared to many traditional financing options, accounts receivable financing is often chosen for its speed, making it a practical solution for businesses that need to improve cash flow quickly.

Where can I get no long-term contract receivables financing?

Many factoring companies and accounts receivable financing providers offer programs with no long-term contracts. These arrangements allow businesses to access working capital from unpaid invoices without committing to lengthy agreements or minimum volume requirements.

When comparing providers, review the contract terms carefully. Some companies advertise flexible financing but still include termination fees, monthly minimums, or automatic renewal clauses. Look for transparent terms, straightforward pricing, and the flexibility to scale financing as your needs change.

For businesses seeking greater control over their funding arrangements, receivables financing with flexible contract terms can provide access to cash flow support without a long-term commitment.

Where can I sell accounts receivable for cash?

Those interested in selling accounts receivable for cash should look for A/R factoring companies, like Charter Capital, an accounts receivable factoring company in Houston. The process works differently from AR financing because the factoring company takes ownership of the invoice, which makes it easier to qualify for, too. Although banks sometimes offer account receivables factoring services as well, their programs are typically designed for larger companies. Dedicated receivable factoring companies are often more flexible and can work with smaller businesses or startups, provided they’re actively generating invoices and have at least some history with their customers.

Is accounts receivable factoring only for small businesses?

No. While small business factoring is popular because smaller companies tend to have reduced reserves and are less likely to qualify for traditional bank loans, factoring is also used by mid-sized companies and sometimes even larger companies when they require immediate capital but lack liquidity or simply don’t want to take on debt.

Why use account receivable factoring or accounts receivable financing?

Accounts receivable funding tools are typically more accessible than traditional bank loans. Even businesses that don’t qualify for loans due to credit challenges or time in business can still receive upfront cash through invoice funding solutions.

Are accounts receivable factoring services and invoice financing the same thing?

No. Invoice financing, also known as accounts receivable financing, is a type of loan where your invoices serve as collateral. It’s a debt instrument. On the other hand, accounts receivable factoring services involve selling the invoices, and the debtor or customer who owes on the invoice then pays the factor directly. It does not create debt for the business leveraging it, as the balance is cleared by the debtor.

What is the accounts receivable financing approval process?

While it’s typically easier to qualify for accounts receivable financing than it is to get a typical bank loan because your invoices serve as collateral, AR financing companies are still collecting payments from you and, therefore, will still consider your credit and time in business as primary approval criteria. Businesses that require more lenient approval criteria will often have an easier time qualifying for factoring, as approval is largely based on the creditworthiness and payment history of the businesses that owe payment on the invoices.

What are the costs of invoice factoring when factoring receivables?

The majority of the cost when factoring receivables is tied to the factoring fee. This is usually set as a factoring rate, which is a percentage of the invoice’s value. Anywhere from one to five percent may be normal, depending on your industry, risk, and other considerations. At Charter Capital, the cost to factor is usually between one and three percent.

How can you get business cash without a traditional bank loan?

If you operate a B2B business that invoices clients and you don’t qualify for a traditional bank loan, don’t want to take on debt, or need cash faster than a bank loan can provide, accounts receivable factoring is a good alternative to bank loans.

Can you finance growth without a loan by factoring receivables?

Yes. Growth often strains cash flow because expenses climb long before client payments come due. By factoring receivables, growing companies can align inflows and outflows and stabilize cash flow. Many also use it to seize business opportunities and accept new or larger projects with confidence.

What are the key types of receivables-based financing?

Those looking for cash flow solutions for unpaid receivables have two core options: factoring and financing. Whereas receivables financing works like a loan and involves debt repayment with interest, factoring involves selling the receivable, so there’s nothing to pay back.

How do I choose between accounts receivable factors?

When comparing factoring receivables companies, look beyond the advertised rate. Consider advance rates, fees, contract terms, funding speed, customer service, and industry experience. The best provider should offer transparent pricing and a program that aligns with your cash flow needs.

It is also important to understand how the factor interacts with your customers, since collections and account management can affect business relationships. Ask about reporting tools, credit services, and any minimum volume requirements.

Because accounts receivables factoring programs can vary significantly, comparing multiple providers is often the best way to identify the right fit. A reputable factor should be able to clearly explain its costs, processes, and contract terms before you commit.

What makes Charter Capital a top receivables factoring company?

Charter Capital stands out as a top receivables factoring company because it combines experience, speed, flexibility, and service. The company has supported businesses with accounts receivables factoring for more than 25 years and offers same-day funding, competitive rates, no long-term contracts, no hidden fees, and no sign-up fees.

Businesses can choose which invoices to factor and when, making it easier to manage cash flow without taking on traditional debt. Charter Capital also provides dedicated account managers, free collections services, free credit reports, digital invoice processing, and high advance rates, giving businesses more than just funding.

What’s the impact of factoring on accounting?

The factoring of receivables affects accounting by converting accounts receivable into cash more quickly. When invoices are factored, the receivable is reduced or removed from the balance sheet and replaced with cash, while any factoring fees are recorded as an expense.

Factoring can improve liquidity and shorten the cash conversion cycle, making it easier to manage working capital. The exact accounting treatment depends on whether the arrangement is structured as a sale of receivables or a financing transaction.

Because accounting requirements can vary, businesses should consult their accountant or financial advisor to ensure receivables factoring is recorded correctly.

What are accounts receivable factoring loans?

Accounts receivable factoring loans are a common term used to describe funding obtained through unpaid invoices, but factoring is not actually a loan. Instead, a business sells its outstanding invoices to a factoring company in exchange for an immediate cash advance.

With accounts receivable financing factoring, approval is typically based on the value of the invoices and the creditworthiness of the customers responsible for paying them. This allows businesses to access working capital without taking on traditional debt.

Factoring is often used to bridge cash flow gaps, cover operating expenses, and support growth while waiting for customers to pay their invoices.

What happens when a factored accounts receivable doesn’t get paid?

What happens when a factored invoice goes unpaid depends on the terms of the factoring agreement. In recourse factoring, the business is typically required to buy back the invoice or replace it with another eligible receivable. In non-recourse factoring, the factoring company may absorb certain losses if the customer cannot pay due to covered credit-related reasons.

Before entering into a factoring of accounts receivable arrangement, it is important to understand how unpaid invoices are handled and what risks remain with your business. Reviewing the agreement carefully can help prevent surprises if a customer fails to pay.