Invoice factoring is a form of business funding where a company sells its unpaid invoices to a factoring company like Charter Capital, receiving immediate cash instead of waiting weeks or months for customer payments. Charter Capital helps businesses maintain steady cash flow to cover payroll, suppliers, and operating expenses—with funding often available within 24 to 48 hours and competitive rates that support growth.

How Can Invoice Factoring Help a Business?

Invoice factoring provides cash to businesses for working capital purposes and helps eliminate cash flow gaps caused by unpaid invoices.

Invoice factoring is also known as invoice funding, accounts receivable funding, and invoice discounting. It’s a flexible and simple way for small businesses to get quick access to working capital.

Regardless of industry, your company depends on constant cash flow in order to stay operational. Unpaid invoices can put pressure on your company’s finances, leaving you with less cash to pay suppliers, payroll, and other unexpected expenses. A deficit in working capital can hinder your business’s ability to reinvest in operations and take advantage of new opportunities, which is something no business owner wants.

Not only this, but customers with unpaid invoices can also be harmful to your employees’ time. If too much time is spent chasing customers for payment, it leaves less time for more important business-day operations. Invoice factoring can be a quick and efficient way to free up working capital and reduce the time you spend chasing customers for late payments.

The factoring process is simple. Invoice factoring involves you selling your unpaid invoices to a factoring company that will, in turn, give you a percentage of the invoice amount upfront. The factoring company will then collect on the invoices for you – freeing up your time for critical business tasks and giving you access to immediate cash flow. Once your client pays the invoice that is outstanding, the factor will remit the remaining balance to your business, minus a factoring fee. Instead of waiting for your customer to pay the invoice they owe, you will get immediate working capital. This capital can be used to fulfill your business needs: whether it be for paying employees and vendors, ordering stock or equipment, or paying your business expenses.

Unlike traditional bank loans, your credit status (or the credit score of your business) typically does not affect whether you will be approved or not. Instead, the factoring company will look at the creditworthiness of your customer to determine any risk involved in collecting on the amounts they owe. The better your customer’s creditworthiness, the higher the invoice percentage the factoring company will be willing to pay you upfront.

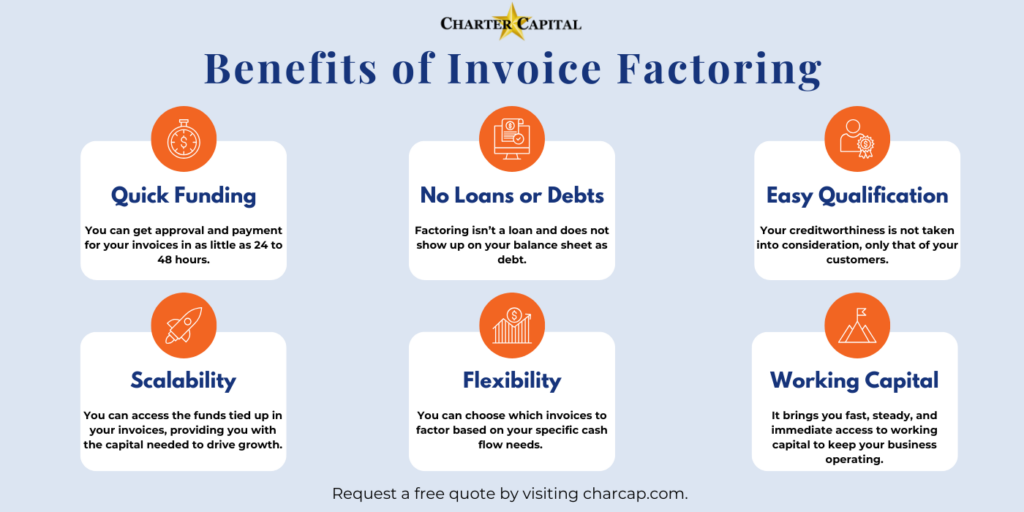

Invoice factoring services also offer a much more immediate cash flow solution. Depending on the factoring company you choose, you can get approval and payment for your invoices in as little as 24 to 48 hours. So, you don’t need to wait the 30, 90, or 120 days that are required with traditional bank financing. To add to the benefits, invoice factoring does not come with the high-interest amounts that plague bank loans.

How Does Invoice Factoring work?

Our three simple steps allow your business to grow, free from cash flow worries.

- 1. Invoice your customers like you normally do.

- 2. Send us the unpaid invoices you want to factor and we will wire you the funds – usually the same day.

- 3. We wait for payment. You get a cash advance to help you grow.

What is the Difference Between Invoice Factoring and Invoice Discounting

In some ways, both invoice factoring and discounting share similarities, but there are some key differences that you should take note of before deciding which service is right for your business.

What is Invoice Discounting?

With invoice discounting, your company is basically borrowing the working capital you need. A financial service provider will pay you the funds you need, secured against your business’s accounts receivable. The lender will then charge you a percentage of the invoice amount as a fee for borrowing the money. With this process, your company is still responsible for collecting payments directly from your customers. Additionally, you will need to continue administering your company’s sales ledger and managing the credit control processes. Generally, customers are unaware that a third-party (i.e., the invoice discounting company) is involved.

How is Invoice Factoring different?

Invoice Factoring is a business transaction whereby a factoring company buys your accounts receivable from you and pays you a specific percentage of their value. A factoring agreement will be drawn up, and per the agreement, your company will hand over its debtor’s book to the factoring firm to collect on the invoices. Your customers will also be made aware of third-party involvement. The factoring company assumes responsibility for managing the debtor administration or credit control processes in-house. A factoring company will perform the invoice processing, credit checks, verify invoice receipt and accuracy, open new customer accounts, assess credit limits to minimize the risk of bad debt, handle collections and payments, and send reminder letters and final demands when necessary. The factoring company can also provide guidance if your business ever needs to settle any disputed accounts.

When considering which service best suits your business, it is important to consider how much your company can spend on credit control services. This is not only in relation to funds but in relation to time as well. Hiring a credit control expert in-house may seem like a good solution. Still, you need to be sure you have the necessary resources and expertise required for hiring, training, managing, and retaining employees in such a specialized field. This is why invoice factoring is more suited to small and medium-sized businesses (who may lack some of these resources) because the factoring company will take over the collections and credit control process, and the costs thereof will be included in the factoring fee. With invoice discounting, on the other hand, the credit control process will still need to be completed in-house.

Invoice Factoring Essentials for Business Cash Flow Enhancement

Invoice factoring, a type of business funding, involves selling outstanding invoices to a third party – a factoring company. This process allows businesses to gain immediate access to a percentage of the invoice amount, enhancing cash flow and operational efficiency. Understanding the factoring process, including how to qualify for invoice factoring and choosing the best invoice factoring companies, is crucial for businesses seeking to optimize their financial strategies.

The factoring company typically advances a significant portion of the invoice amount, with the client responsible for paying the invoice directly to the factoring firm. The cost of invoice factoring varies depending on the factoring company and the agreement terms. Businesses considering this option should understand the difference between invoice factoring and invoice funding, as well as the pros and cons of invoice factoring.

One key aspect of invoice factoring is the collection of the invoice. When a client fails to pay their invoice, the factoring company takes on the responsibility for collecting it, which can be a major advantage for businesses that want to avoid the hassle of chasing payments. Invoice factoring is often a fast, effective solution for businesses needing quick access to funds, especially when traditional financing options are not feasible.

A recourse factoring agreement is a common arrangement where the business retains the risk if the client does not pay the invoice. Conversely, non-recourse factoring transfers this risk to the factoring company. The choice between these two types depends on the level of risk the business is willing to take and the cost implications.

When working with an invoice factoring company, it’s essential to consider factors like the percentage of the invoice that will be advanced, the fees charged, and the company’s experience and reputation in collecting the invoice. The right factoring company can be a great asset, providing not just financial support but also valuable services in managing credit and collections.

Moreover, invoice factoring is a strategic option for businesses that work with customers who may take longer to pay. It provides a flexible and efficient way to manage cash flow and can be a good solution for businesses looking to grow or stabilize their operations. With the right approach and understanding of how factoring works, businesses can leverage invoice factoring as a key component of their financial toolkit.

What Types of Industries Use Factoring to Improve Cash Flow?

- Trucking & Freight

- Staffing Agencies

- Manufacturing Companies

- Security Firms

- Consulting & Service Firms

- Oil and Gas Services

- Construction

Why Factor Your Invoices?

Waiting for outstanding invoices to be paid is one of the most frustrating aspects of running a business. If you don’t qualify for traditional small business loans, you face a major cash-flow gap between billing your customers and getting paid. Cash flow problems are one of the main reasons for the lack of business success.

Using Invoice Factoring as a form of business funding is especially important for small businesses, so you can invest in needed equipment, pay vendors, or meet any needed business expenses like payroll. The alternative, of course, is to go after your customer for invoice payments and delay everything else while the cash is tied up in the collection process. Instead, an invoice factoring agreement guarantees you will see cash for your invoices. At Charter Capital, our simple and easy accounts receivable funding process gives you a debt-free cash flow solution – with no waiting. For instance, trucking companies often face extended payment cycles. By leveraging freight bill factoring, they receive immediate advances on unpaid invoices and can bridge cash flow gaps.

Factor Invoices With a Trusted Partner

It is always important to ensure you are using the services of a trusted, experienced, and reliable factoring company. As your customers will be made aware of third-party involvement in the collections on their accounts, a reliable factoring company will be able to put their minds at ease and dispel any concerns they may have regarding the process. A well-established factoring company, like Charter Capital, will know exactly how to professionally liaise with your customers and clearly explain the advantages that come with its involvement in the process.

Charter Capital has earned a reputation for assisting companies just like yours for more than 20 years. Long-term customer relationships and client referrals illustrate the tailored results of our personal, one-on-one service.

What are the benefits of using an Invoice Factoring Company?

The benefits are abundant! For starters, invoice factoring:

| It is an alternative source of business funding that eliminates many of the roadblocks posed by traditional bank loans. |

| It does not require a business plan or tax statements, unlike a traditional bank loan. |

| Factoring isn’t a loan and does not show up on your balance sheet as debt. It is a financial transaction between a business and Charter Capital, and therefore does not include a bank. |

| It frees up your working capital. For many companies or small business owners, a significant amount of capital is tied up in accounts receivable. Invoice factoring companies may convert these assets into immediate cash so you can meet expenses. |

| It frees up your valuable time. Outsourcing your accounts receivable to a factoring facility lets you focus on selling, producing, and growing your business. |

| It brings you fast, steady, and immediate access to working capital to keep your business operating at optimal cash performance. |

Your creditworthiness is not taken into consideration, only that of your customers. So, even if you have filed for bankruptcy in the past, you may still be able to qualify for invoice factoring when you may not qualify for a traditional bank loan.

Are Invoice Factoring Services Suitable For All Businesses?

If your company is struggling because of extended credit terms or if it’s an uphill battle to obtain other types of business credit. Invoice funding

can be ideal for your company, no matter if it’s large or small.

What are Some Common Invoice Factoring Fees?

If you are researching factoring services for your company, one of the most probable questions you will ask is, “How much does invoice factoring cost?”

There isn’t necessarily a straight answer to this question because the factoring cost is dependent on multiple factors, including how many invoices your company wants to factor, how long your customers will take to pay, and the total value of the invoices your company will factor on a monthly basis. It also depends on which factoring company you choose.

Here are some of the common fees and terms you may see in your factoring agreement:

Application/Due Diligence Fees:

This is an upfront fee that is only charged by some factors and not by others. This fee is typically paid to the factor once you have received the money for your invoices. It is, however, important to keep in mind that factoring companies that do not charge this fee may recover it by increasing the amount of your initial factoring fee.

Termination Fees:

This is a small fee that is usually paid to the factor if a small business chooses to end the factoring agreement. This fee is typically a percentage of the credit line from the factoring company. The rate paid varies based on the factoring company you use and the terms outlined in your agreement. This is why it is essential to read your factoring agreement thoroughly so you know what fees and costs you may be liable for. A reliable factoring company should be more than willing to answer any questions you may have, so don’t be afraid to ask.

Monthly and Weekly Fees:

Again, this fee is dependent on the terms outlined in your factoring agreement. Depending on your contract, you may be required to pay monthly or weekly maintenance fees. Payment options and fees may vary between factoring companies. Some factors may provide you with a smaller percentage taken weekly rather than a larger percentage taken monthly. Even with a higher rate, the monthly fee could end up being lower in the end.

Customer Limit:

With factoring agreements, the small business gets an overall credit line from a factor; however, the factor will not want to tie up too much money in invoices from a single customer. Invoices from one customer can only make up a certain percentage of the credit line, so it is important to know that percentage when entering an agreement.

Discount Fee:

This is the cost that you will be charged in return for the factoring company paying for your invoices in advance. It can vary anywhere from 1.5% to 5% of the invoice value each month. Be sure to check the discount fee with your factor, as this fee is largely dependent on which company you choose. Charter Capital, for example, offers factoring fees as low as 1%.

Invoice Factoring Fee:

For every 30 days that your invoices are outstanding beyond the initial 30 days covered by the advance discount fee, you can expect an additional 2–3% charge. In some cases, the fee may be prorated daily, while others may charge on a 10-day basis. This all depends on your factoring agreement and whether you have chosen recourse or non-recourse factoring, as well as the creditworthiness of your customers. Look for factoring companies that offer the most transparency with regard to their fees.

Credit Check Fees:

As previously mentioned, the creditworthiness of your customers needs to be determined before a factoring company will enter into an agreement with you. In order to see if your customers meet certain standards, credit checks will be done. This is not a fee charged by all factoring companies, so be sure to read your contract carefully to determine whether or not your business will be liable.

What is the Difference Between Recourse Factoring and Non-Recourse Factoring?

The type of invoice factoring service you choose should reflect your business needs.

Non-recourse factoring is typically slightly more expensive than recourse factoring because the factor will assume all the risk of collecting the debt, making it a lower-risk option for your business if you cannot absorb the cost of unpaid invoices. While the fees may be more expensive for this option, there are benefits. With the factoring company accepting insolvent risk, your business will reduce bad debt and increase cash flow, even if your customer never pays the invoice.

Recourse Factoring is suitable for businesses that are confident that their customers will pay their invoices. This confidence should come from past experiences that your customers are reliable when it comes to their payments, not an assumption or hope that they will pay. This is because if your customers do not pay their invoices, you will need to repay the factor (buy back your invoices) or replace the noncollectable. Remember the invoice with one that is equal to or greater than its value. So, while the fees may be cheaper, the risk will still fall on your company. This option is often preferable to larger companies that can afford to return the funds they received from the factor if their customer fails to pay their invoice and it is determined noncollectable. Keep in mind that the factoring company will conduct credit checks on your customers to determine if you meet the qualification criteria.

A recourse plan is a good option if your customers are reliable in paying you. You will pay less and not have to worry about customers’ nonpayment. While a non-recourse plan can provide additional protection for your company, it is not necessary if credit monitoring procedures are in place to minimize the risk of customers’ non-payment.

Looking For Helpful Invoice Factoring Resources?

We want to help your business grow and have gathered some helpful resources to answer all of your questions.

What Makes Charter Capital Different?

- Competitive Rates

- No Hidden Fees

- No “Maintenance” Fees

- Professional Staff

- Dedicated Account Executive

- Personalized Service

- Residuals Paid Weekly

- Assistance With Credit Decisions

- Advance Rates Up To 90% or more

- Daily Reporting of Receipts

- No Long-Term Contracts

- Same-Day Funding

- Customized Programs

Ready?

What sets Charter Capital apart from other factoring companies is that we do not require you to have perfect credit to get an affordable factoring rate, and we are a direct source of funds. In addition, our requirements are easy to meet, making it a simple process to get funded directly from us in a timely manner.

So, there’s no reason to wait! Call us toll-free at 1-855-912-7671 or contact us today to find out how easy it is to get started with invoice factoring. One of our account representatives will be happy to assist you and answer any questions you may have about invoice factoring