Rapid growth may seem like every entrepreneur’s dream, but it often creates more problems than it solves. In fact, an analysis of Inc.’s 500 fastest-growing private companies shows that five to eight years after making the list, fast growers perform worse than their counterparts, Inc. reports. Perhaps more concerning, two-thirds shrink, stagnate, or outright fail.

On this page, we’ll explore why this happens, including some of the pitfalls of rapid growth, red flags that signify you may have a problem, and how leveraging factoring for business growth challenges can help.

Financial Challenges Associated with Rapid Business Growth

More often than not, it’s the financial challenges associated with rapid business growth that create issues and seep into virtually all business activities.

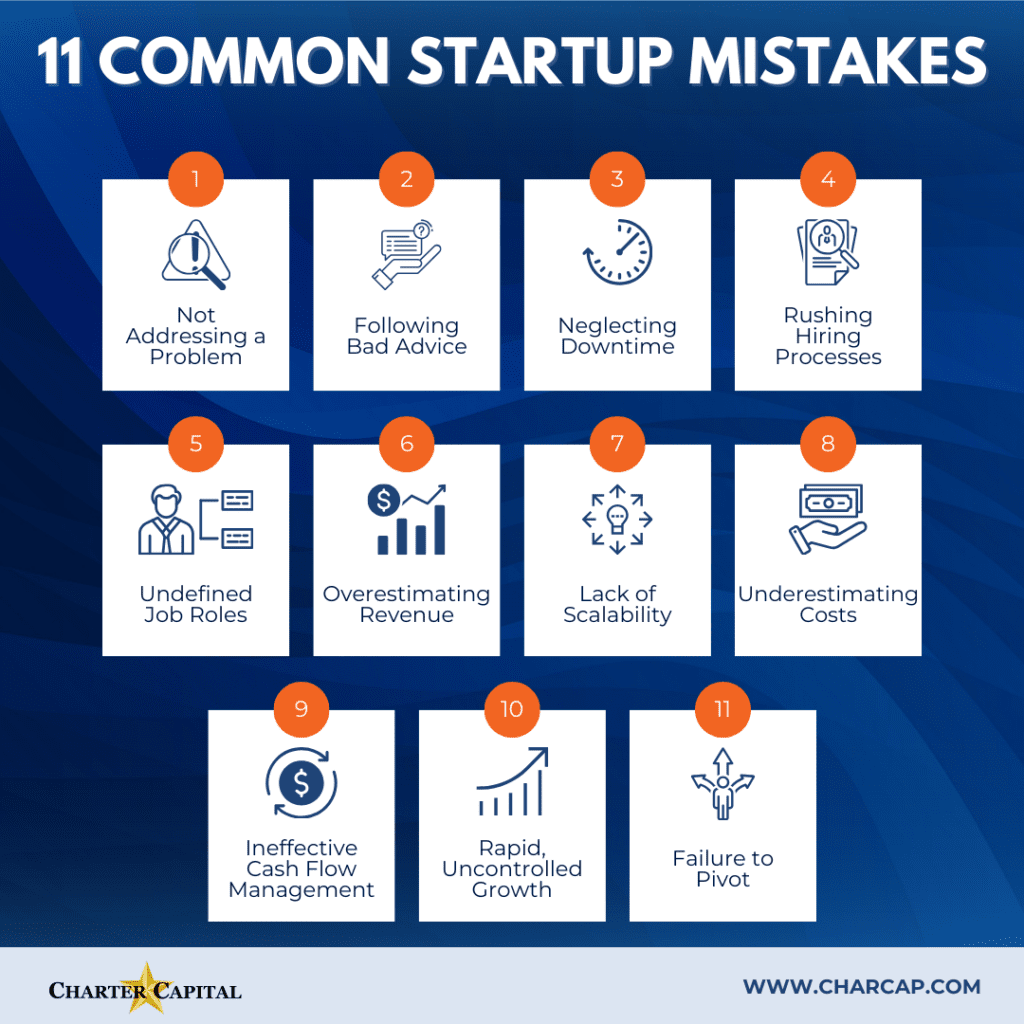

Overhead Increases

Businesses may anticipate increased expenses for things like inventory, but they don’t always see increases in overhead expenses coming. For instance, utility bills, materials, and salary expenses often increase. Many businesses must also upgrade their space to have more room for storage, manufacturing, or back-office processes as well.

Poor Management

Business leaders, especially small business owners, wear many hats during the startup phase. You’re not merely the strategic visionary. You’re managing daily activities, the head of HR, the person chasing unpaid invoices, and so forth. It’s easy to become overwhelmed in these situations and impossible to ensure that each task gets the attention it deserves.

Many red flags can signify management is going downhill. However, you’re likely having issues in this area if your business experiences surprises, such as unexpected peaks in unpaid invoices or emergency cash flow shortfalls that need immediate attention.

Trouble Meeting Demand

If your business is struggling to fulfill orders that have already been placed, or you’re turning down work because you lack the resources to fulfill them, it’s safe to say you’re having trouble meeting demand.

Without a proper business expansion plan, this usually results in one or more of the following scenarios:

- Reduced Quality: Brands ramp up production to meet demand, but quality decreases.

- Increased Customer Complaints: Customers become upset with long waits and poor quality and begin to complain.

- Increased Attrition: Without a strong customer retention strategy, the business begins losing customers.

- Reduced Volume: Demand for products and services declines because customer expectations are unmet.

People Problems

Rapidly growing businesses often fail to define their company structure, or it changes so much that people don’t know what to expect. For instance, people may report to multiple managers or may not receive the communication they need to perform their job well. This creates low morale, burnout, and employee attrition, impacting all business aspects.

To fill these gaps and those created by business growth, the company hires rapidly, often bringing people on who are not a good fit for the role or company culture.

Red flags your business is dealing with this include an increase in HR complaints, poor results from employee surveys, and high attrition rates.

Too Much Focus on the Short-Term

Many business owners, especially first-time founders, learn on the job. That can work when things are slow, particularly if the owner builds a strong team with experienced professionals. However, it’s virtually impossible to keep up with all the changes and adjust strategies when everything changes quickly.

- Decisions Based on Feeling: Rather than making decisions based on thorough analysis, decisions are based on feelings and personal desires. For instance, you might develop a product or service based on what you believe people want or how you’d use something instead of what others do.

- R&D Focused on Short-Term Gains: Rather than developing strategies your business can leverage in the long run or grow into, you spend your R&D investments on immediate gains.

- Borrowing without Planning: Rather than developing a long-term growth strategy that puts loans toward vetted growth initiatives, the business borrows large sums or stacks loans that are used for immediate needs that it cannot pay off.

Red flags can vary here, though businesses often struggle with cash flow management and meeting customer demands. There’s also often considerable waste. For instance, the business may not fully utilize its team or space, and inventory may go unused.

Problematic Cash Flow Management

All the issues outlined so far can make it difficult to predict cash flow and create and stick to budgets. Over 80 percent of small business failures are tied to poor cash flow management, Small Business Trends reports.

Leveraging Factoring for Business Growth

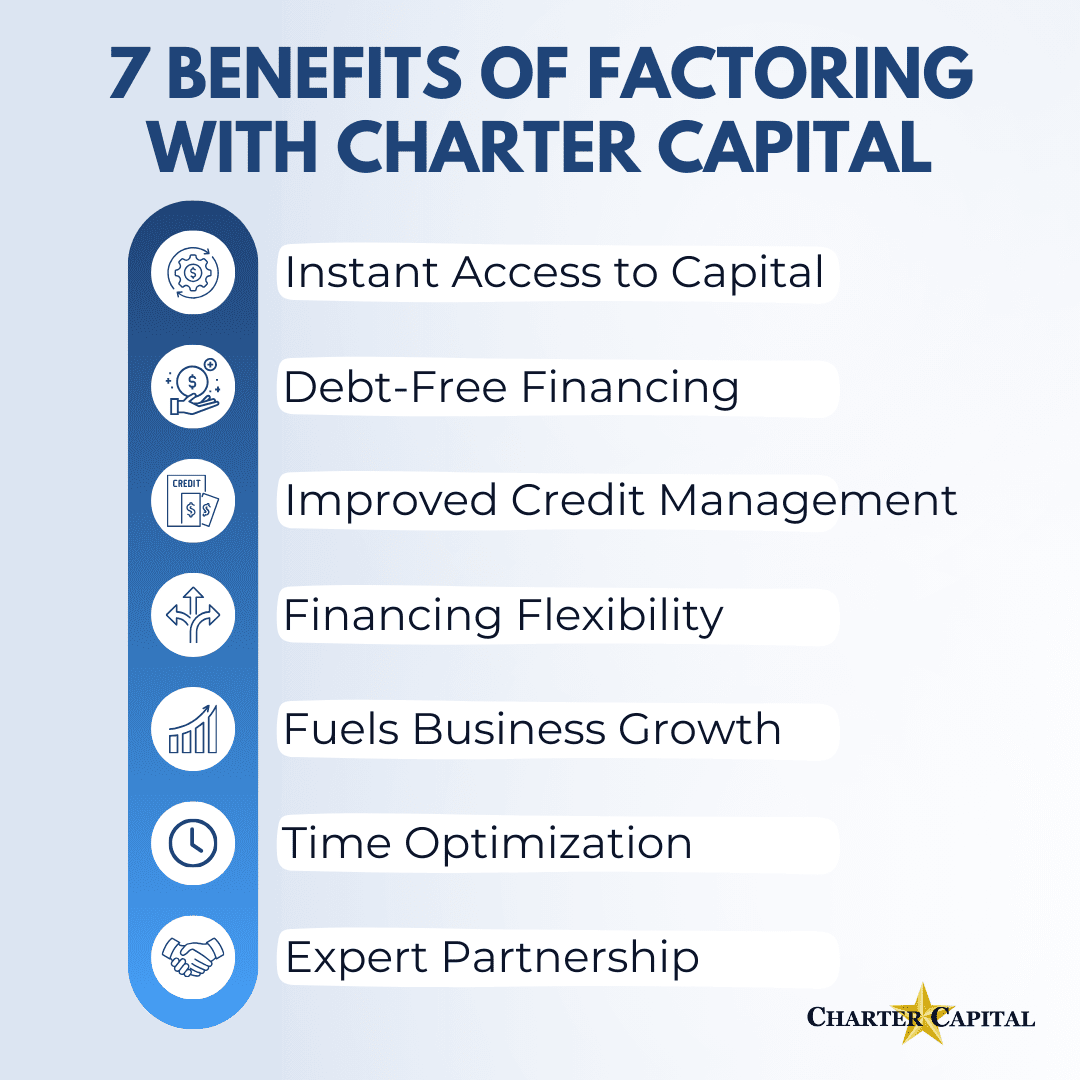

While there are many financial solutions businesses can leverage, invoice factoring offers unique benefits that make it ideal for growth funding.

Rather than taking out a loan that your business may struggle to repay later, factoring provides instant payment on your outstanding B2B or B2G invoices.

Rapid growth can create complex financial challenges for any business, including those in the security industry. This is where security factoring comes into play as a reliable solution. By leveraging the value of unpaid invoices, security companies can secure immediate funds needed to meet payroll, hire additional guards, and handle increased operational costs. Factoring offers a flexible way to maintain financial stability and avoid the pitfalls of debt, making it a preferred choice for firms experiencing rapid expansion.

Similarly, staffing agencies facing rapid expansion can benefit from payroll funding through invoice factoring, ensuring they have the necessary working capital to cover wages without cash flow disruptions.

Factoring Works Even if You’re Still Building Credit

Most business funding options only work for businesses with strong credit scores. Invoice factoring doesn’t rely on your credit and may even help you improve your credit score.

You Receive Working Capital Instantly

Factoring makes it easy to cover unexpected expenses because you can tap into it as needed, and funding is instant. While this typically means you’ll receive payment within a couple of days, Charter Capital goes the extra mile and can provide same-day payments.

It Does Not Create Debt

It’s very easy for rapidly growing businesses to become buried in debt, especially when volume begins to decrease. At this stage, it eats up a significant portion of profit even though the business may only be paying interest and fees and not paying down the principal. Factoring helps companies avoid this fate because it doesn’t create debt. The balance is paid off when your customer pays their invoice.

Factoring Simplifies Cash Flow Management

Effective cash flow management begins with creating accurate financial projections. That’s difficult to do when cash inflows are unpredictable and outflows are rising. Invoice factoring takes the guesswork out of it by stabilizing cash flow. You know precisely when you’ll get paid, so you can create a budget and stick to it.

You Can Focus More

Decision-making falters when business leaders are stressed and tackling too many things. When you factor, your factoring company collects balances to save you the time and trouble of chasing invoices. You’re also likely to feel less stressed because issues like customer bad debt are reduced, and you can focus on business strategy more.

Get Started with Factoring for Business Growth

With more than 20 years of experience, tailored services to meet your unique needs and competitive rates, Charter Capital can help. If your business is facing challenges due to rapid growth, request a complimentary invoice factoring quote.