Did you know that just two in five small businesses that apply for funding are approved for all the funding they seek, according to the latest Small Business Credit Survey? Nearly a quarter are completely denied, and the rest land somewhere in between; in that awkward place where they get some of the cash requested, but not enough to do what they actually need to do. While this may seem grim, there are still lots of often-overlooked business funding tips and tricks. In this guide, we’ll walk you through what you can do before applying, while applying, and after funding to help ensure you get the most capital possible and maximize its use.

Business Funding Tips for the Preparation Stage

If you’re trying to improve your odds of getting a small business loan, start by ensuring your business looks like a responsible borrower on paper at least a few months before you begin applying.

Improve Your Credit Profile

Naturally, your credit score is a major deciding factor if you’re seeking traditional funding. Unlike personal credit scores that are managed by Equifax, Experian, and TransUnion, which range from around 300 to over 800, your business credit score can be anywhere from 0 to 100. You’ll still have different scores based on the credit bureau, but in this case, it will be Equifax, Experian, and Dun & Bradstreet (D&B).

To build small business credit:

- Register: Ensure you’ve selected a proper business structure and filed the paperwork to make your business a legal entity.

- Check Your Profiles: Check with each bureau to confirm the info they have about you is accurate and follow up on a regular basis to ensure it stays that way.

- Pay Bills Early: To get the best possible D&B score, you actually have to pay vendors and other creditors early, not just on time.

- Build Where You Can: Establish trade lines with your suppliers and leverage credit in small amounts that you can pay off quickly to begin building your score.

- Minimize Debt: Avoid taking on debt and reduce debt ratios whenever possible, so funding companies see you’re managing finances wisely and can afford payments.

Organize Your Financial Documents

Have clean, up-to-date records. Lenders and investors want to see tax returns, profit and loss statements, and cash flow forecasts.

Know Your Numbers

Build business financial literacy skills. This will help you improve your numbers and boost lender confidence. Explore key areas like tax planning, bookkeeping, budgeting, forecasting, and financial statement analysis.

Diversify Revenue Streams

Businesses with multiple revenue streams are typically more stable because they’re not reliant on a single area. If customer demand, supply chains, or other areas shift, you have something else to fall back on. Because of this, the perceived risk of lending to your business is often reduced, and you can often secure larger funding amounts.

Build Strong Banking Relationships Before Seeking Business Loans

It’s often easier to access lines of credit or negotiate terms if you build business relationships with key professionals like bankers before you need funds.

Funding Strategies for the Application Stage

Once you have a strong foundation, explore various funding options to find the right fit and start applying. The following tips will help improve your chances of success.

Match the Funding to the Need

Different goals call for individualized tools. Consider using lines of credit for short-term cash flow management, invoice factoring for similar purposes, as well as for slow invoices or seasonal cash flow concerns, and save term loans for equipment or expansion.

Apply For Small Business Funding Before You Need Working Capital

Explore working capital options before you’re in a bind and apply before you need funding. This serves two major purposes. First, your business will look better on paper when it’s financially strong, so you’re more likely to get approved and qualify for the level of funding you need. Secondly, this approach allows you breathing room to make informed choices. If you wait until you’re unsure if you can cover payroll or order supplies, you’re more likely to accept whatever terms you’re offered, even if they’re not great and won’t benefit your business in the long run.

An option like small business invoice factoring is often ideal in these situations, as you can get approved and ensure funding is available ahead of time, and then not use it or pay any fees unless you actually factor an invoice. This can help you manage costs better and speed up the funding timeline if you face an unexpected expense or hit a bump in the road later.

Have a Professional Business Plan

A well-written plan with market analysis, financial projections, and an outline of how you plan to use the funds speaks to your professionalism and demonstrates that any money invested in your company will be well spent, which boosts the confidence of lenders and investors. Alternative funding companies also appreciate seeing business plans.

Explore Alternative Funding Options

By default, most businesses turn to bank loans for funding. However, approval rates are even lower for traditional business loans than other options, with two-thirds of applicants receiving denials, according to the Small Business Credit Survey.

Moreover, there are some nuances between “good debt vs. bad debt.” For instance, if taking on debt allows you to increase the net worth of your business or has future value, it often fits in the “good debt” category. But if it doesn’t add to your net worth or could potentially leave you with nothing to show for your payments, it’s likely in the “bad debt” category. When these situations apply, consider alternative financing.

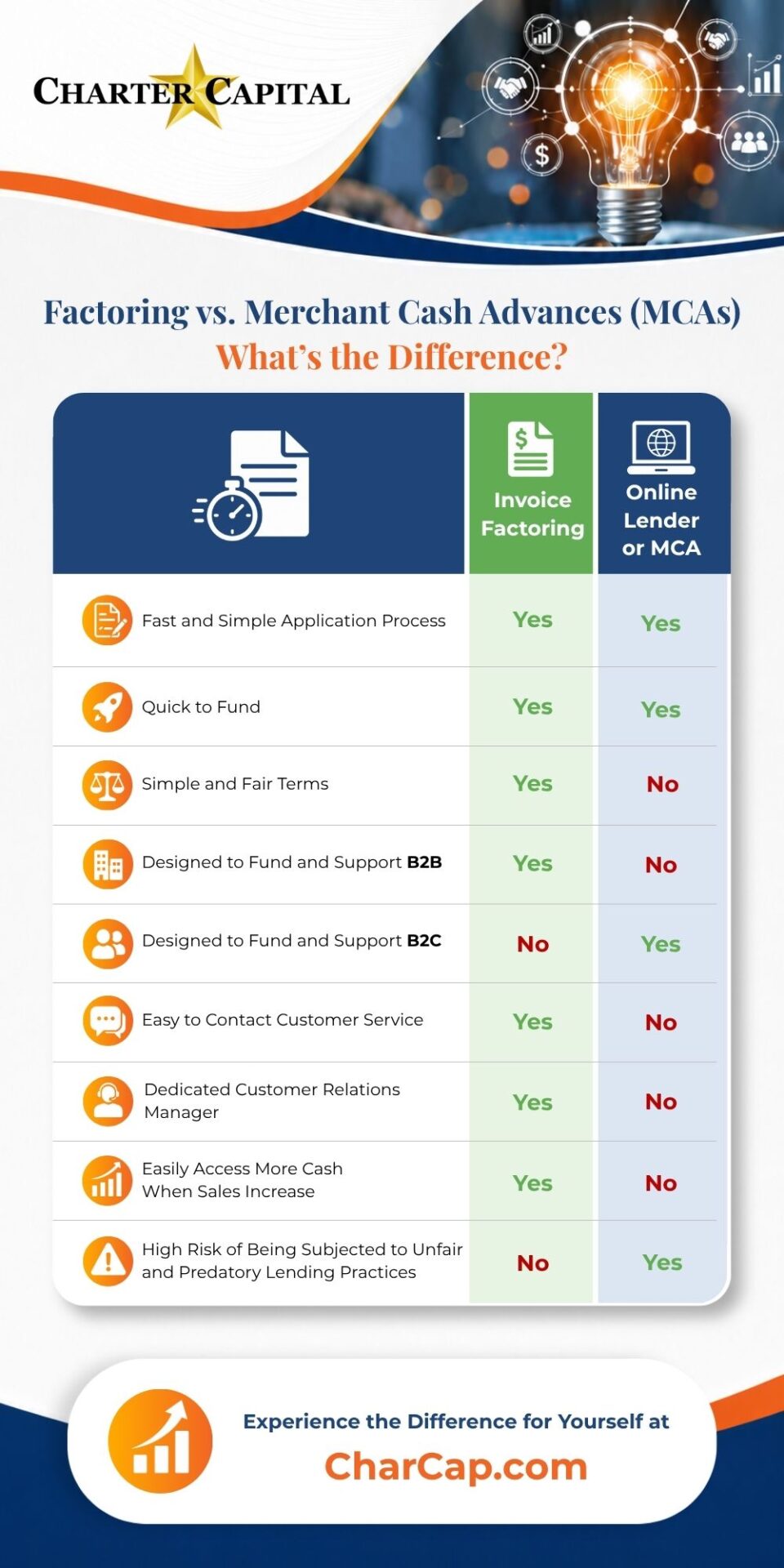

That might mean using venture capital for startup financing or tapping into merchant cash advances (MCAs). However, it’s important to be mindful of how these choices impact your equity and profitability, as equity dilution may hinder your ability to make decisions, and MCAs tend to come with high costs.

That might mean using venture capital for startup financing or tapping into merchant cash advances (MCAs). However, it’s important to be mindful of how these choices impact your equity and profitability, as equity dilution may hinder your ability to make decisions, and MCAs tend to come with high costs.

Invoice factoring also fits into the alternative funding category, but it’s different because it’s not a loan, so there’s no debt to pay off, and it doesn’t reduce your equity. It’s an advance on your unpaid B2B invoices.

Keep Personal Finances in Good Shape

Many lenders still look at personal credit scores. Especially for small businesses, your financial habits impact perceived risk.

Maximizing Business Capital Post-Funding

At this stage, you’ve strengthened your financial position, applied for funding, and received at least some of the money you needed. Here’s how to ensure that cash goes as far as possible.

Use Funds Strategically

It can be difficult to stay focused on your business goals as competing priorities emerge. However, it’s essential to use your funds for their intended purpose. It may help to use a project management system like Wrike or Asana to break your big-picture goals into smaller milestones, so you always have your goals at the forefront of your mind and stay on track.

Burnout and decision fatigue can also lead to unnecessary spending. Delegate tasks whenever possible to ensure you have the bandwidth to oversee your business activities strategically.

Reinvest in Growth-Generating Activities

Prioritize return on investment (ROI). Invest your funds in areas that will help you maximize profitability, tap into business growth resources, or expand your business.

Monitor Loan Covenants and Triggers

Some loans have reporting or financial performance requirements. Keep up with them to avoid defaults or higher rates.

Track ROI on Every Dollar

Measure the effectiveness of your funding use. This can help you justify the need for funding later and adjust your strategy in real time.

Maintain Communication with Lenders and Investors

Transparent updates build trust, which makes renewals, extensions, and future fundraising much easier.

Position Your Business for Future Growth and Valuation

Getting the funding you need is a strong step forward, but if you’re thinking about long-term growth, expansion, or even selling your business one day, it’s important to consider how today’s funding choices shape your future.

Strong customer retention, recurring revenue, and scalable operations can increase the valuation of your business. Lenders and potential buyers often look at key performance indicators (KPIs) like profit margins, customer lifetime value, and cash flow.

By using funding to strengthen these areas now, you not only improve current performance, you also set your business up for long-term success and future opportunities.

Maximize Your Business Funding with Invoice Factoring

Invoice factoring is unique, so it helps businesses in lots of different ways. For instance, it’s accessible, even to businesses that don’t have strong credit or are just starting out. This means you can use it as your core source of funding even if other avenues are closed.

While you’re using it, it can help you maintain healthy cash flow and engage in activities that boost your credit, which may make it easier to qualify for traditional bank loans and other credit-dependent funding options down the road.

Many businesses also leverage it to fill gaps left by other sources. For instance, if you need $100,000 to purchase equipment but only get a $50,000 loan, you can factor $50,000 worth of invoices to reach the total sum needed and start generating more revenue faster.

If you’d like to make the most of your business funding and explore invoice factoring, request a complimentary rate quote.