Navigating Your Small Business Financing Options & Cash Advances

When it comes to finding the right loan for your small business, the landscape can be bewildering, especially when considering options like an SBA loan or business credit cards. With the advent of online lenders offering small business loans and financing options, entrepreneurs now have a wealth of opportunities at their fingertips. Whether you’re seeking a merchant cash advance, a business line of credit, or the best small business loans available, understanding your options is critical. The key is to find a financing option that not only meets your immediate business needs but also supports your long-term growth, such as a business credit card for smaller expenses or a substantial SBA loan for larger projects. Small business financing can take various forms, from business term loans to business cash advances, each with its advantages. For those looking to apply for a small business loan online, the application process has become more accessible than ever, offering a streamlined path to funding options like SBA loans and business credit. However, it’s essential to weigh the pros and cons of each type of small business financing, including interest rates, repayment terms, and eligibility requirements. By doing so, you can find a business loan that aligns with your cash flow and helps you grow your business. Remember, the best business loan is one that fits your specific needs, enabling you to capitalize on opportunities without overextending your financial resources.

Online Small Business Loans/Cash Advances

As a small business owner, it’s not news to you that companies need capital to get started, to buy essential equipment and inventory, to grow and if everything goes according to plan, prosper. And it shouldn’t be a surprise to you that sources of capital can sometimes be hard to come by for small businesses.

But what you may not know is that an increasingly popular new source of small business funding – quick online business loans – might not be the boon cash-starved entrepreneurs had hoped would be their salvation.

The Internet has certainly been a boon for small business owners, especially smaller ones. It has often enabled the startups to effectively compete with the giants of commerce in terms of creating a market presence. It has also helped small businesses establish cost-effective ways to do business with their customers and eliminate the expense of a big sales force, brick-and-mortar stores or offices. Over the past several years, a new phenomenon has been sweeping the Web that promises small businesses greater access to much-needed capital through online loans and cash advances.

Small business entrepreneurs once had a limited choice on raising capital to start a company, to keep one going or to help it grow. They could tap into their own savings, ask friends or family for money, fill out an application with the Small Business Administration (SBA), or walk into a neighborhood bank and seek a loan.

Related Article: It’s Small Companies, Not Big Business, That Create Jobs

Some of these methods are easier than others. The easiest, of course, is tapping into personal savings. However, how many people have sufficient savings to keep loaning their businesses money? Asking friends or family for funds can be problematic. A federal loan means you have to deal with a slow government bureaucracy. Going to the bank entails proving your business plan and your creditworthiness (credit score), and banks are becoming more risk-averse, meaning they’re loaning less and less to small businesses. If your credit check shows your business as bad credit risk, it will be near impossible to get a line of credit through a bank.

Enter the online loan industry. Now you can fill out a form on a website and if approved, quickly get much-needed cash for your business. Sounds great, doesn’t it? Perhaps it may even sound too good to be true? And we’ve all heard the old adage that famously says, “If it sounds too good to be true, it probably is.”

Is that the case when it comes to online small business loans? Is a cash advance a bad thing? That depends on factors such as your business credit and time in business. How fast do you need the money, what price are you willing to pay for it, and are you willing to place yourself at risk?

Taking out an online business loan is often much easier than applying for a loan from the SBA or a traditional lender. There are fewer forms, fewer questions, and less documentation. The sites are typically written in easy-to-understand language and can be quickly navigated by anyone. So that may be a competitive plus when compared to the SBA or most banks, but at what cost?

There are potential pitfalls small business owners need to keep in mind should they decide to pursue a business loan online.

For one, fees and interest rates generally tend to be much higher for online loans than for traditional loans from a bank. There are often more fees attached to the online loan than loans from other sources.

“Caveat emptor”—let the buyer beware. The internet is swamped with alternative lenders using gimmicks to gain attention, making it challenging to find a reputable business lender. One such gimmick is to express the interest rate in terms of simple interest as opposed to APR (annual percentage rate) – a more realistic measure of the cost of funds. Expressing the interest rate as “simple” rather than as APR can be confusing, even misleading because the actual interest rate can be much more expensive than it appears.

Repayment terms are another important item to consider. Many online loans have set repayment provisions, and these provisions could wind up making the loan more of a hindrance down the road than a help. If you are expecting a traditional monthly payment plan, for example, you may be surprised to learn the online lender you’ve taken a loan from actually requires payment every week, or in the worst cases, even daily. Can your cash flow handle these strict requirements?

Finally, there is the security issue. News reports come out almost daily about online scams of all kinds. Just because someone has put up a website advertising online business loans does not automatically mean it’s a legitimate firm. There’s the possibility it’s a fly-by-night outfit looking to steal your information and good name for their own nefarious uses or a lead gather who will then sell it to online lenders.

If you are going to use an online lender to obtain a small business loan, here are a few ideas on how to protect your company and find a safe lender. First, make sure the lender has a real physical address, which is crucial whether you’re looking to get a small business loan or open a business bank account. If the site does not provide one, run away. If the site does give an address, use tools like Google Street View to confirm it is an actual location and not an empty field.

Next, search for third-party verification from such sources as the Better Business Bureau and other rating services. One additional tip is to find out who owns the website, how long they’ve been around, and if they are actually an online lender. You can do this using WHOIS.

It’s always best to do strict due diligence on the lender and read all the fine print before taking out any loan, be it online or through a traditional source. Not doing so could put your small business at risk. Yes, small business loans are increasingly harder to come by through traditional lending sources and businesses need capital, sometimes quite quick capital. But by investing a little time, you can save yourself and your businesses from tripping over avoidable pitfalls.

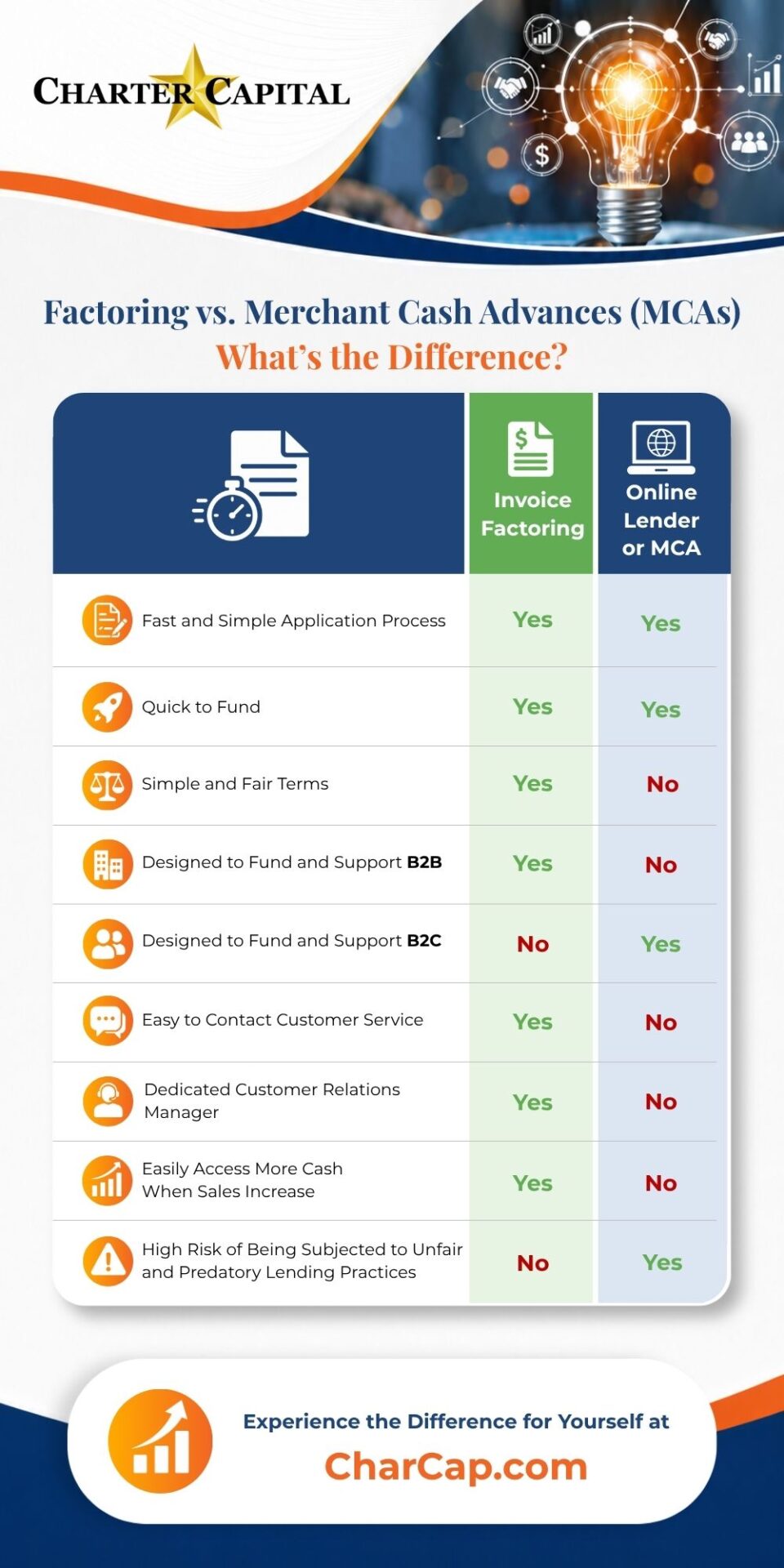

Why Factoring is a Smart Financing Choice for Small Businesses

When it comes to small business financing, factoring emerges as a superior option for many businesses due to its unique advantages over traditional and online loans. Unlike conventional loans, which often require extensive credit checks and collateral and can take time to be approved, factoring provides immediate access to funds by allowing businesses to sell their outstanding invoices at a discount to a third party, known as a factor. This method is especially beneficial for businesses with strong sales but slow-paying customers, as it improves cash flow without the need for taking on new debt.

When it comes to small business financing, factoring emerges as a superior option for many businesses due to its unique advantages over traditional and online loans. Unlike conventional loans, which often require extensive credit checks and collateral and can take time to be approved, factoring provides immediate access to funds by allowing businesses to sell their outstanding invoices at a discount to a third party, known as a factor. This method is especially beneficial for businesses with strong sales but slow-paying customers, as it improves cash flow without the need for taking on new debt.

Factoring stands out for several reasons:

- Immediate Liquidity: Factoring converts accounts receivable into immediate working capital, enabling businesses to cover operational costs, take advantage of growth opportunities, and manage cash flow gaps without waiting for customer payments.

- Credit Extension Not Required: Unlike business loans, which depend heavily on the business and owner’s creditworthiness, factoring focuses on the creditworthiness of the business’s customers. This makes it an accessible option for new or rapidly growing businesses that may not qualify for traditional financing.

- Reduces Administrative Burden: The factor often assumes responsibility for managing the receivables, including collections from customers, which can reduce administrative overhead and allow business owners to focus more on core business activities and growth strategies.

- Flexibility: Factoring agreements can be more flexible than traditional loan contracts, with businesses able to choose which invoices to factor and when. This provides businesses with more control over their finances and avoids the long-term commitments often associated with loans.

- No Additional Debt: Since factoring is not a loan, it does not add to a company’s debt load. This is crucial for maintaining a healthy balance sheet and can be especially advantageous for businesses looking to keep their debt-to-equity ratios low.

By embracing factoring, small businesses can navigate the challenges of growth and cash flow management with greater ease and flexibility. This financing option supports sustainable business operations by offering a practical solution to the common problem of delayed invoice payments, ensuring that businesses can continue to invest in their growth and stability without the burdens often associated with more traditional financing routes.

- What is an Invoice Factoring Broker? - July 17, 2022

- 7 Tips for Buying Out a Business Partner or Majority Owner - May 13, 2022

- 6 Leadership Secrets Every Small Business Owner Should Know - December 9, 2021