A Merchant Cash Advance (MCA) seems attractive. You get the large sum of money you need to keep your company running, and the lenders take an agreed upon amount from your bank account for so many weeks until the loan is paid. But beware, the reality is that MCAs are a sale of a share of your company’s future profits.

What is a Merchant Cash Advance?

For many companies, a Merchant Cash Advance (MCA) might initially appear as the quick cash solution they’ve been searching for. These advances, provided by merchant cash advance companies, promise an upfront sum of money. However, they’re tied to a portion of your company’s future credit card sales. Essentially, it’s financing based on future promises rather than concrete achievements. And while the idea of immediate capital is enticing, it’s crucial to understand the terrain. MCAs often come attached with high interest rates. So, if your company’s sales don’t meet the optimistic projections, you could be navigating a tough road of unexpectedly hefty payments.

Why Choose Invoice Factoring as a Financing Option

In the vast world of financing, companies might find themselves drawn to the promises made by merchant cash advance providers. But a more detailed look could illuminate the undeniable benefits of invoice factoring. Unlike the somewhat speculative nature of MCAs, invoice factoring companies offer advances grounded in the here and now: your unpaid invoices. This means your company is leaning on tangible, completed sales. Such an approach not only guarantees more predictable rates but also avoids the looming shadows of MCAs’ high interest rates. The process of applying for invoice factoring? It’s as efficient as MCAs, but without the dicey risks of penalties should sales predictions fall short. To put it plainly, invoice factoring lets companies maximize the value of their current invoices, ensuring a smooth cash flow that’s not at the mercy of tomorrow’s sales forecasts. So before your company gets too enamored with MCAs, it’s wise to stack up the benefits side by side. You might find that invoice factoring presents a clearer, steadier route to financing.

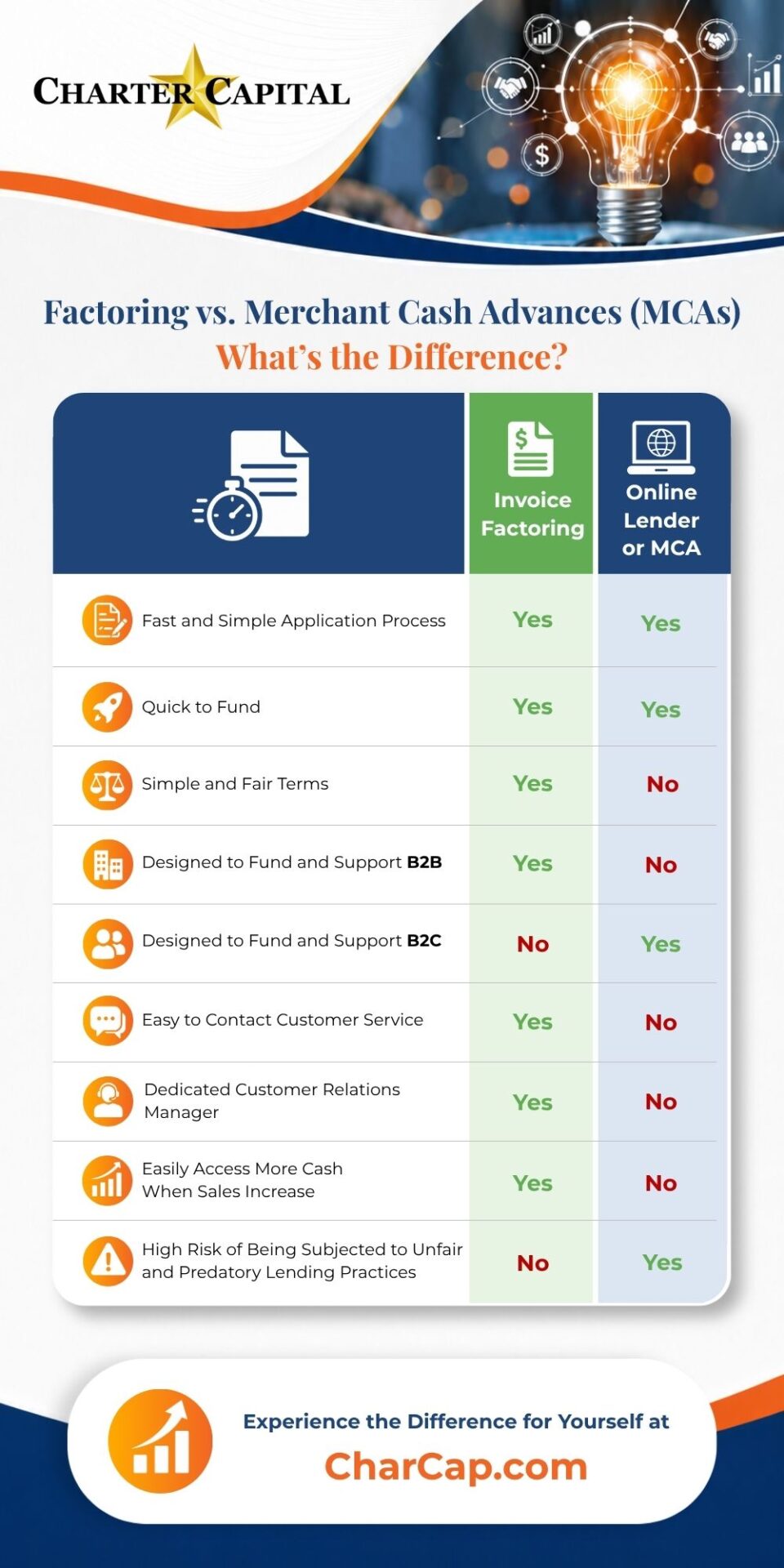

The Strategic Choice Between Invoice Factoring and Merchant Cash Advances

Navigating the financing options available to small business owners, particularly within sectors with longer payment cycles, demands a strategic approach toensure both immediate cash flow needs and long-term financial stability are addressed. When considering merchant cash advances (MCAs) versus invoice factoring, it’s crucial to understand how each impacts your business’s bottom line. MCAs, while offering a lump sum of cash based on future credit and debit card sales, often come with stringent repayment terms, including daily or weekly deductions from your sales, which can significantly affect your working capital. This form of financing may seem attractive for businesses in need of immediate cash, but the higher costs and risk of non-payment due to fluctuating sales underscore the importance of considering alternative funding sources.

On the other hand, invoice factoring presents a compelling financing option for small business owners seeking to enhance their cash flow without the burden of traditional loans or the unpredictability of MCAs. By selling your unpaid invoices to factoring companies, you receive advance funds, often within one business day, giving you the working capital you need to operate and grow without waiting for clients to pay. Unlike MCAs, invoice factoring provides flexibility with repayment terms and doesn’t hinge on your daily credit card sales, making it a better alternative for managing your accounts receivable efficiently. Moreover, the application process for factoring is straightforward, with a focus on your invoices’ value rather than your business’s credit score, offering a financing solution that supports business development and allows you to take advantage of opportunities without the looming pressure of repaying a lump sum plus fees and interest.

Merchant Cash Advances vs. Invoice Factoring

Invoice factoring makes more sense for businesses that don’t deal with a high volume of credit card transactions. For instance, trucking businesses will typically find freight factoring to be more accessible, while security guard firms can tap into security factoring.

With invoice factoring, the advance you receive on your invoices is based on actual sales rather than a prediction of future sales. This means your business will benefit from the same quick cash flow and simplified approval process as an MCA with significantly less risk.

Since merchant cash advances use a prediction rather than an actual dollar amount, you may be forced to make huge payments if your sales don’t meet your projections (usually with much higher interest rates than invoice factoring rates). Payments may even continue beyond the period in which you generate revenue, which could pose a larger problem. In contrast to merchant cash advance brokers, who charge you both the payment amount and a crippling interest rate, invoice factoring companies only charge a small percentage of the invoice amount (the factoring fee).

You may also be able to benefit from the back-office services provided by invoice factoring companies, including billing and collections since they purchase your unpaid invoices and collect payments directly from your customers.

Make sure you understand the short- and long-term implications of taking out a merchant cash advance before you commit. In desperate situations, their interest rates may seem worthwhile but be aware that anything that looks too good to be true, usually is.

At Charter Capital, we help trucking companies grow with freight factoring and customer-focused services.

Give us a call at 1-877-960-1818.

- What is an Invoice Factoring Broker? - July 17, 2022

- 7 Tips for Buying Out a Business Partner or Majority Owner - May 13, 2022

- 6 Leadership Secrets Every Small Business Owner Should Know - December 9, 2021